Payday loans are short-term, high-interest loans you can qualify for with no credit check. They’re supposed to help people with bad credit get financing, but they usually do more harm than good. Unfortunately, each state gets to decide whether to allow or prohibit them within their borders. Here’s how the Alabama payday loan laws work.

Table of Contents

Payday lending status in Alabama: Legal

The Alabama payday loan laws place restrictions on the industry in the state, including capping the allowable principal amount and interest rates. Unfortunately, the limits they impose don’t do much to protect consumers.

Lenders are still well within their rights to charge triple-digit annual percentage rates (APRs). As a result, the predatory loan industry continues to flourish in Alabama.

READ MORE: States where payday loans are illegal

Stuck in payday debt?

If you’re an Alabama resident, DebtHammer may be able to help.

Loan terms, debt limits, and collection limits in Alabama

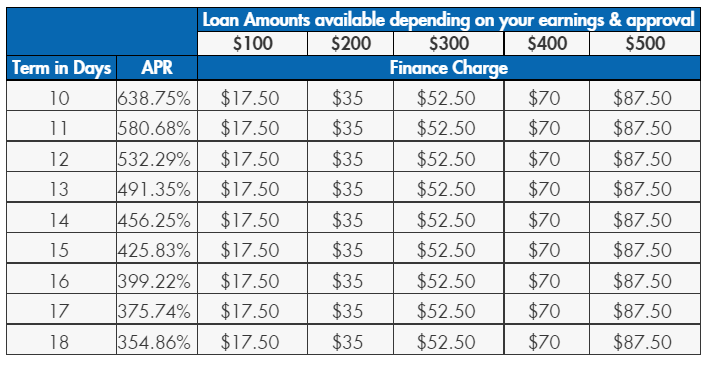

- Maximum loan amount: $500

- Maximum Interest Rate (APR): 456.25% on a 14-day, $100 loan

- Minimum loan term: 10 days

- Maximum loan term: 31 days

- Number of rollovers allowed: One

- Number of outstanding loans allowed: Any, as long as the total amount advanced is less than $500

- Installment option: No

- Cooling-off period: One business day after a rollover

- Finance charges: 17.5% of the amount advanced

- Collection charges: $30 non-sufficient funds (NSF) fee; Court costs and an attorney’s fee up to 15% of the principal amount and finance charge

- Criminal action: Prohibited

Payday lenders consistently trap vulnerable borrowers with thin financial margins and poor credit in a cycle of debt. They have to resort to debt to cover surprise expenses, and their borrowing options are usually limited to lenders that don’t check credit scores. That drives them straight into the hands of payday lenders.

Because payday loans are so expensive and have short repayment terms, it’s difficult for most borrowers to save up enough money to pay them back before they come due. When that happens, they usually pay a fee to extend the due date or take out another payday loan, which only delays the inevitable.

In states that don’t restrict rollovers, borrowers can end up paying extra fees for months on end without ever making progress on their debts. The Alabama payday loan laws only allow one rollover and limits outstanding balances to $500, but that doesn’t solve the root of the problem.

READ MORE: Alabama debt relief and resources

Alabama payday loan laws: How they stack up

Despite the many experts that have pointed out how likely payday loans are to trap you in debt rather than solve your financial problems, the industry remains legal in most parts of the United States.

Payday loans are illegal in Arizona, Arkansas, Colorado, Connecticut, Georgia, Maryland, Massachusetts, Montana, Nebraska, New Hampshire, New Jersey, New Mexico (as of Jan. 1, 2023), New York, North Carolina, Pennsylvania, South Dakota, Vermont, West Virginia and the District of Columbia.

Some state governments believe that payday lenders provide a valuable service to consumers who need financing but struggle with bad credit. Therefore, they refuse to restrict the industry.

Other states have tried to eliminate payday lending but failed to create effective regulations. Payday lenders are notorious for skirting the law and generally take advantage of any loopholes they can find.

Alabama falls into the latter category. There have been attempts to regulate payday lenders in the state into submission, but lobbyists have defeated all attempts to eliminate the industry. Here’s a more in-depth explanation of how their regulations work in practice.

READ MORE: How to get out of a payday loan nightmare

Maximum loan amount in Alabama

The maximum payday loan amount in Alabama is $500. The limit applies regardless of the number of lenders or transactions involved.

For example, if you have one $300 payday loan, you can only borrow up to $200 more, whether you work with the same lender or another one. Payday lenders are supposed to verify how much you have in outstanding payday loan debt before entering into a contract with you, though they might not always do so.

READ MORE: Payday loan consolidation and relief that works

What is the statute of limitations on a payday loan in Alabama?

A statute of limitations on debt is a law that defines how long a lender or debt collector has the right to initiate legal proceedings to collect a delinquent debt. The length varies significantly between states and sometimes even within them for different types of debt.

The limit is six years for written contracts like payday loans in Alabama.

Rates, fees, and other charge limits in Alabama

The Alabama payday loan laws limit finance charges to 17.5% of the amount advanced. That means you’ll generally pay $17.50 in fees for every $100 you borrow from a payday lender.

For example, to take out a $300 payday loan for two weeks, you’d have to pay $52.50 in fees. That means your post-dated check would have to be for $352.50 total, which works out to a 456.25% APR.

If you fail to pay your loan back, lenders can take you to court to collect. If they win the case, you’ll also have to pay their lawyer’s fees up to 15% of the face amount of your post-dated check.

Alabama lenders can also charge up to $30 in NSF fees if your post-dated check or their direct debit fails because you don’t have enough money in your bank account to cover it.

Maximum term for a payday loan in Alabama

The Alabama payday loan laws prohibit repayment terms from being longer than 31 days. However, you can extend it with a single rollover, which essentially doubles the life of the loan.

If you still can’t pay what you owe after the rollover, the lender can offer you an extended payment plan that involves four equal monthly installments. If you don’t accept the payment plan within 15 days of the lender notifying you, they can take you to court.

In addition, payday loans can’t have a repayment term of fewer than ten days. Many lenders offer products starting at two weeks.

How many payday loans can you have in Michigan?

No law limits the number of payday loans a borrower can have simultaneously, but if you need more than one, you’ll likely have to use a different lender. Though payday lenders don’t report loans to the three major credit bureaus, they do have their own reporting system, so if you already have a couple of outstanding payday loans — or have defaulted on a previous payday loan — the new lender will typically be aware.

There’s also no overall limit to the number of payday loans you can have, so once you pay off your original loan, you’re immediately eligible for a new loan. However, this isn’t recommended.

READ MORE: Can you have multiple payday loans?

Are tribal loans legal in Alabama?

Native American tribes are legally sovereign nations located within the United States. As a result, they don’t have to abide by state regulations, even if they’re technically within that state’s borders.

Tribal lenders partner with Native American tribes to share their tribal immunity and use it as an excuse to charge finance fees above state limits. Usually, that involves filling out some paperwork and filing forms that make the tribe the official owner of the lending operation.

However, some state courts have ruled that paperwork isn’t enough to prove that these tribal lenders are legitimate arms of the tribe. That would strip the lenders of their immunity and force them to follow state lending laws.

Unfortunately, Alabama hasn’t taken that stance yet. The Alabama State Banking Department issued a consumer alert in 2019 that tribal lenders may not be subject to their jurisdiction. As a result, tribal lenders are still legal in the state.

READ MORE: Is my payday loan lender licensed?

Consumer information

The Alabama State Banking Department charters, regulates, and examines financial institutions in the state. It’s also responsible for licensing and regulating lenders, including mortgage brokers, pawnshops, and payday lenders.

The Bureau of Loans is the department division in charge of enforcing the Alabama payday loan laws that protect consumers. It can take steps to discipline payday lenders that violate the Alabama Deferred Presentment Services Act, including imposing financial penalties or stripping licensees of their right to practice.

READ MORE: How to get out of high-interest tribal loans

Where to make a complaint

The Alabama State Banking Department is the best place to make a complaint about a payday lender in Alabama if you suspect they’ve broken the law. Here’s how you can get in touch with them:

- Regulator: Alabama State Banking Department

- Physical Address: 401 Adams Avenue, Suite 680, Montgomery, AL 36104-4350

- Mailing Address: P.O. Box 4600, Montgomery, AL 36103-4600

- Phone: (334)242-3452 or (866)465-2279

- Link to website: http://www.banking.alabama.gov/complaint.aspx

It’s also a good idea to submit a complaint to the Consumer Financial Protection Bureau (CFPB). The CFPB is a federal organization that protects consumers from predatory financial institutions, including payday lenders.

Number of Alabama consumer complaints by issue

These statistics are all according to the CFPB Consumer Complaint Database.

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 84 |

| Struggling to pay your loan | 71 |

| Problem when making payments | 33 |

| Getting the loan | 26 |

| Received a loan you didn’t apply for | 23 |

| Can’t contact lender or servicer | 23 |

| Can’t stop withdrawals from your bank account | 19 |

| Problem with the payoff process at the end of the loan | 17 |

| Incorrect information on your report | 17 |

| Loan payment wasn’t credited to your account | 16 |

| Money was taken from your bank account on the wrong day or for the wrong amount | 10 |

| Problem with a credit reporting company’s investigation into an existing problem | 8 |

| Problem with additional add-on products or services | 6 |

| Was approved for a loan, but didn’t receive money | 6 |

| Applied for loan/did not receive money | 5 |

| Credit monitoring or identity theft protection services | 4 |

| Improper use of your report | 3 |

| Vehicle was repossessed or sold the vehicle | 1 |

| Property was damaged or destroyed property | 1 |

Source: CFPB website

The top consumer complaint about lenders in Alabama is that they charge unexpected fees or interest. That’s often the case in states that allow the payday lending industry to operate freely since their rates are generally orders of magnitude higher than other forms of borrowing.

The second most common complaint is similar. Almost as many people reported that they’re struggling to keep up with their loans. That’s also unsurprising since payday loans are more expensive than many borrowers can afford.

The most complained about lender in Alabama: Enova International, Inc.

Enova International, Inc. is the most complained about lender in Alabama. It’s the parent company for CashNetUSA and NetCredit, both of which provide loans with predatory interest rates.

They’re not payday lenders, but they might as well be. CashNetUSA provides lines of credit with APRS between 149% and 299%. NetCredit offers personal loans with APRs up to 65%.

Those are cheaper than most payday loan rates, but they’re potentially more dangerous because personal loans have higher principal balances and longer repayment terms. For example, a 49-month, $6,300 personal loan from NetCredit would cost $5,900 in interest at 36% APR.

Most common complaints about Enova International, Inc.

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 11 |

| Struggling to pay your loan | 4 |

| Getting the loan | 3 |

| Money was taken from your bank account on the wrong day or for the wrong amount | 2 |

| Received a loan you didn’t apply for | 2 |

| Loan payment wasn’t credited to your account | 1 |

| Problem with a credit reporting company’s investigation into an existing problem | 1 |

Source: CFPB website

Unsurprisingly, the most common complaint about Enova International, Inc. is that they charge unexpected fees and interest. That’s probably partially because their subsidiaries aren’t as forthcoming as they should be about costs.

For example, NetCredit discloses APRs and total monthly payment amounts. However, they don’t share what portion of those monthly payments would go toward interest or tally up the total cost of their loans. You have to do the math yourself.

Top 10 most complained about payday lenders

| Lender | Number of Complaints Since 2013 |

| Enova International, Inc. | 24 |

| Community Choice Financial, Inc. | 19 |

| Advance America, Cash Advance Centers, Inc. | 16 |

| Thaxton Investment Corporation | 15 |

| CURO Intermediate Holdings | 15 |

| Tower Loan of Mississippi, Inc. | 14 |

| OneMain Financial, LLC. | 13 |

| CNG Financial Corporation | 12 |

| Big Picture Loans, LLC | 9 |

Source: CFPB website

The CFPB has received more complaints about Enova International, Inc. than any other lender in the state, but the gap between them and the other top offenders is relatively thin.

Community Choice Financial, Inc. and Advance America are short by less than ten complaints each. Both companies offer traditional payday loans at the maximum allowable APR in Alabama.

Advance America also offers installment loans. They’re not quite as expensive on a percentage rate basis, but the principal balances are much higher. As a result, they have the potential to be even more dangerous than a payday loan.

For example, a 14-day payday loan for $500 has a max APR of 456.25% in Alabama. A two-year personal loan for $3,000 from Advance America has an APR of 168.93%. However, the finance charges are $87.50 and $7,564.88, respectively.

The most complained about tribal lender in Alabama: Big Picture Loans, LLC

The most complained about tribal lender in Alabama is Big Picture Loans, LLC. They operate online instead of setting up storefronts, which has contributed to them becoming the top offender in most parts of the United States.

As a tribal lender, they charge far more than what states typically allow, including Alabama. They offer loans from $200 to $5,000 that can last anywhere from four to 18 months. Their APRs can be as high as 699%, and new customers can’t qualify for anything below 200%.

Most Common Complaints About Big Picture Loans, LLC

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 3 |

| Problem with the payoff process at the end of the loan | 3 |

| Received a loan you didn’t apply for | 2 |

| Can’t stop withdrawals from your bank account | 1 |

Source: CFPB website

The most common complaint people make about Big Picture Loans in Alabama is that they charge fees or interest you don’t expect. That makes sense since their rates can reach almost 700% APR.

Somewhat more surprisingly, there are just as many complaints about Big Picture Loans’ payoff process, which is disturbing. If you can’t complete your final payment, you’ll incur additional penalties and remain trapped in debt even longer.

Payday loan statistics in Alabama

- Alabama ranks as the 17th state for the most overall payday loan complaints.

- Alabama ranks as the 7th state for the most payday loan complaints per capita.

- There have been 18,281 payday loan-related complaints made to the CFPB since 2013―373 of these complaints originated from Alabama.

- The estimated total population in Alabama is 4,903,185 people.

- There are 7.6073 payday loan complaints per 100,000 people in Alabama.

- The most popular reason for submitting a payday loan complaint is “Charged fees or interest you didn’t expect.”

READ MORE: Payday loan debt statistics

Historical timeline of payday loans in Alabama

Alabama has had a long history with the payday lending industry. Regulators have tried to prevent predatory lenders from taking advantage of consumers numerous times, but the lenders have always managed to stay one step ahead.

Here’s an overview of the most significant events affecting the Alabama payday loan laws over the years.

- Late 1990s: The Alabama Attorney General issued an opinion that said the Alabama Small Loan Act covered payday lenders. Subsequently, the Alabama State Banking Department issued cease and desist orders to lenders violating the legislation. The lenders generally ignored them.

- 2002: Lender lobbyists managed to modify the Alabama Small Loan Act to allow up to 190% APR for payday lenders.

- 2003: The Deferred Presentment Act passed, which raised the allowable APRs even higher. The Act still governs the payday lending industry in 2021.

- 2013: The Alabama State Banking Department proposed a database that would track lender activities to reduce rule-breaking. Payday lenders sued them to try and prevent its creation, but they failed.

Fortunately, current sentiments in Alabama are trending firmly against payday loans. In 2018, the Public Affairs Research Council of Alabama (PARCA) commissioned a poll that showed the following results:

- 84% of voters believe payday loans should be restricted or banned.

- 75% of voters want to cap interest rates at 36% and raise the minimum repayment term to 30 days.

- 80% of voters believe protecting borrowers is more important than payday lenders’ profits.

Hopefully, these trends indicate that reform is coming that will effectively defang payday loans in Alabama. A 36% rate cap is the standard for eliminating predatory lending, and it usually causes payday lenders to close up shop.

Flashback: An Alabama payday loan story

While many payday lenders argue that they provide a valuable service to vulnerable consumers, their loans are undeniably responsible for ruining many of their customers’ finances.

Some level of callousness is a prerequisite for entering into the business. As a result, payday lenders fight tooth and nail against anything that would limit their ability to take advantage of consumers.

A notable example occurred in 2013 when the Alabama State Banking Department proposed a centralized database to track payday loan transactions.

Its primary purpose was to enforce the legislation limiting payday loan borrowing amounts and rollovers. Without a database to track transactions, there’s no way for state regulators to confirm lenders are obeying those laws, and they’d likely break them constantly.

As you’d expect, the industry fought desperately to block the database by suing the Alabama State Banking Department. The cost of the database to the lenders was negligible at just $0.68 per transaction for the first year, so the only real reason to block it would be so they could continue skirting the law.

The bottom line: Should you take out a payday loan in Alabama?

Payday lenders usually target individuals who need fast cash to pay for an unexpected expense like their car breaking down. People who aren’t hardpressed for money can take the time to secure more affordable financing.

Unfortunately, payday loans don’t really solve these kinds of financial emergencies anyway. They only delay them for the life of the loan, after which you’ll have to pay the same amount as the cost of the original crisis plus a significant finance charge.

As a result, you should avoid taking out a payday loan in Alabama or any state whenever possible. If you need short-term financing, you’re usually better off using a free cash advance app like Earnin. It lets you borrow against your earned but unpaid W-2 wages at no cost.

Of course, the only long-term solution is to reach a financial equilibrium where you’re saving a healthy percentage of your paycheck and have an emergency fund in the bank. If you need help starting that journey, contact DebtHammer today.