Despite its predatory reputation, payday lending still occurs frequently across America. Because the industry is regulated by state officials — not the federal government — the rules are inconsistent. Here’s what you should know about the Colorado payday loan laws if you live in the state.

Table of Contents

Payday lending status in Colorado: Prohibited

Colorado’s Proposition 111, which passed in 2018, included legislation that effectively curtailed the payday loan industry in the state. Not only did it cap interest rates at a 36% annual percentage rate (APR), but it also required that the loans have a minimum repayment term of six months.

However, payday lenders found workarounds and loopholes to bypass Prop. 111 by replacing payday loans with so-called “alternative charge loans,” which were not subject to the same consumer protections. In 2023, state legislators passed House Bill 23-1229, which closed that workaround.

H.B. 23-1229 also ensures that out-of-state, state-chartered banks must follow Colorado’s lending laws when lending to Coloradans.

“Voters overwhelmingly approved Prop 111 to protect against predatory payday loans in Colorado, but until now, a loophole has allowed some lenders to continue related high-interest lending practices,” said Rep. Mike Weissman, D-Aurora, sponsor of HB23-1229. “With this law going into effect, we’re aligning Colorado law with the will of the voters and saving hardworking Coloradans money on these financial products.”

READ MORE: States where payday loans are illegal

Stuck in payday debt?

DebtHammer may be able to help.

Loan terms, debt limits, and collection limits in Colorado

- Maximum loan amount: $500

- Maximum Interest Rate (APR): 36%

- Minimum loan term: 180 days (six months)

- Maximum loan term: N/A

- Number of rollovers allowed: One

- Number of outstanding loans allowed: Any, as long as the aggregate balance is less than $500

- Cooling-off period: 30 days

- Finance charges: Origination fees up to 20% of the first $300, plus 7.5% of any amounts above $300. Maintenance fees of up to $7.50 per $100 loaned, not to exceed $30 per month. Total is not to exceed 36% APR.

- Collection fees: One non-sufficient funds (NSF) fee up to $25

- Criminal action: Prohibited

Because of their high interest rates and short repayment terms, payday loans force borrowers to come up with sums of money that can be all but impossible for them. When people can’t pay them off, they pay a rollover fee to extend the loan.

Because it’s even less likely that they’ll be able to afford the next loan payment, they end up rolling payday loans over repeatedly and effectively getting stuck.

The Colorado payday loan laws defang that trap. Thanks to the state restrictions, loans are much more affordable, which reduces the likelihood of default. Even if borrowers do default, they can only perform one rollover.

Feel free to take a look at the original legislation for more details.

Colorado payday loan laws: How they stack up

Colorado is currently one of twenty or so states that have prohibited payday loans within their borders. That puts them in the minority, with roughly two-thirds of the United States either actively permitting payday loans or failing to ban them.

Unfortunately, payday lenders tenaciously resist attempts to eliminate their usurious practices. Because of the nation’s division over the issue and payday lenders’ unfortunate endurance, it may be a while before the United States eliminates the industry.

If you live in Colorado, here’s a closer look at the state’s payday loan laws to make sure you know your rights.

READ MORE: How to get out of payday loan debt

Maximum loan amount in Colorado

In Colorado, payday lenders may not loan a borrower more than $500 in aggregate. That means if you already have one payday loan for $400, neither your existing lender nor a second one could give you any more than another $100 in payday loans.

Note that in this case, both the principal proceeds and finance charges are part of the loan balance. That means your lender can only give you a loan for $450 if they want to roll a $50 origination fee into the financed amount.

READ MORE: Payday loan consolidation and relief that works

Rates, fees, and other charge limits in Colorado

Article 3.1 of the Consumer Credit Code governs payday loans (deferred deposit transactions), but it doesn’t technically forbid them. In fact, it states that payday lenders can charge up to 45% interest per year.

However, Section 2 supersedes this rule by requiring that all supervised loans (which includes payday loans) can cost no more than 36% APR. As a result, the 45% rule is moot.

Other limits in Section 3.1 are still often relevant, though, including limitations on origination fees and maintenance charges.

Origination fees can be no more than 20% of the first $300 of the loan and 7.5% of amounts above that. Because payday loans can’t exceed $500, the maximum origination fee is $75 (20% of $300 is $60, and 7.5% of $200 is $15).

Monthly maintenance charges can be no more than $7.50 per $100 loaned, not to exceed $30 total. For example, a $500 loan would cost $37.50 per month at $7.50 per $100, but the $30 limit prevents it.

Maximum term for a payday loan in Colorado

The Colorado payday loan laws do not stipulate any maximum repayment term. However, they require that borrowers receive a minimum of six months to pay, which is much longer than a typical payday loan in other states.

What is the statute of limitations on a payday loan in Colorado?

A statute of limitations is the amount of time in which a debt collector can sue you over unpaid debts. When this period expires, the court can’t order you to repay your old debt.

In Colorado, the statute of limitations for most debts is six years. Auto loans are the exception. The statute of limitations for auto loans in Colorado is four years.

Are tribal loans legal in Colorado?

Native American tribes are sovereign nations in the United States. That means they’re generally immune to state regulations and it’s hard to sue them for breaching the laws of the states they reside in, though they usually follow applicable federal laws.

Tribal lenders are short-term loan providers that partner with Native tribes to try and share in their tribal immunity. They use that as an excuse to sidestep the regulations meant to protect consumers, such as the rate restrictions on payday loans. In Colorado, the issue is particularly complicated.

H.B. 23-1229 specifies that interest rates established by the state’s “Uniform Consumer Credit Code” apply to all consumer credit transactions. However, the issue is complicated by tribal sovereignty, and courts have taken different approaches.

Rulings in Colorado have held that, in certain circumstances, sovereign immunity applies to payday loans. This means tribal lending is technically legal in Colorado. There are no prohibitions on lending services from a Native American reservation, and tribal lenders still have a presence in the state.

However, lenders must be licensed by the Colorado Division of Banking. Many tribal lenders are not licensed, and if your loan is from an unlicensed lender, it may not be legally collectible.

If you suspect that you’ve borrowed money from an unlicensed lender, please contact a Legal Aid attorney for advice.

READ MORE: Is my payday lender licensed in my state?

Consumer information

The Colorado Office of the Attorney General is in charge of enforcing payday loan laws within the state. Their Consumer Credit Unit manages licensure and registration programs for companies and individuals involved in consumer lending, debt collection, debt management, and student loan servicing.

Supervised lenders, including payday lenders, fall under their purview. The Consumer Credit Unit enforces the terms and conditions in the Colorado Uniform Consumer Credit Code, which sets forth the current restrictions on payday loan interest rates, fees, and repayment terms.

The office investigates complaints about these lenders and takes the appropriate disciplinary or legal action against those who fail to abide by the law, which may include fining or disbanding them.

Where to make a complaint

The Colorado Office of the Attorney General is also the best place to register a complaint about illegal payday lending activities within the state. Here’s the contact information:

- Regulator: Colorado Office of the Attorney General

- Address: 1300 Broadway 10th Floor, Denver, CO 80203

- Phone: 720-508-6000

- Link to website: https://coag.gov/file-complaint/

Consumers can also submit a complaint to the Consumer Financial Protection Bureau (CFPB). They are the federal government’s organization dedicated to helping consumers with financial issues, including problems with payday lenders.

Number of Colorado consumer complaints by issue

These statistics are all according to the CFPB Consumer Complaint Database.

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 76 |

| Struggling to pay your loan | 23 |

| Can’t contact the lender | 21 |

| Getting the loan | 20 |

| Problem with the payoff process at the end of the loan | 17 |

| Problem when making payments | 15 |

| Loan payment wasn’t credited to your account | 14 |

| Received a loan you didn’t apply for | 11 |

| Incorrect information on your report | 9 |

| Applied for loan/did not receive money | 7 |

| Can’t stop charges to a bank account | 6 |

| Problem with additional add-on products or services | 3 |

| Money was taken from your bank account on the wrong day or for the wrong amount | 3 |

| Improper use of your report | 1 |

| Unable to get your credit report or credit score | 1 |

| Unable to get your credit report or credit score | 1 |

| Problem with a credit reporting company’s investigation into an existing problem | 1 |

Source: CFPB website

The most complained about lender in Colorado: Populus Financial Group, Inc.

Populus Financial Group is the lender that consumers complain about the most in Colorado. They’re a large and well-established company with four subordinate brands:

- Ace Cash Express

- Flare Account

- Elite

- Porte

The most problematic of these is Ace Cash Express. While the other three focus on mobile banking services, Ace is a national payday and short-term installment loan provider.

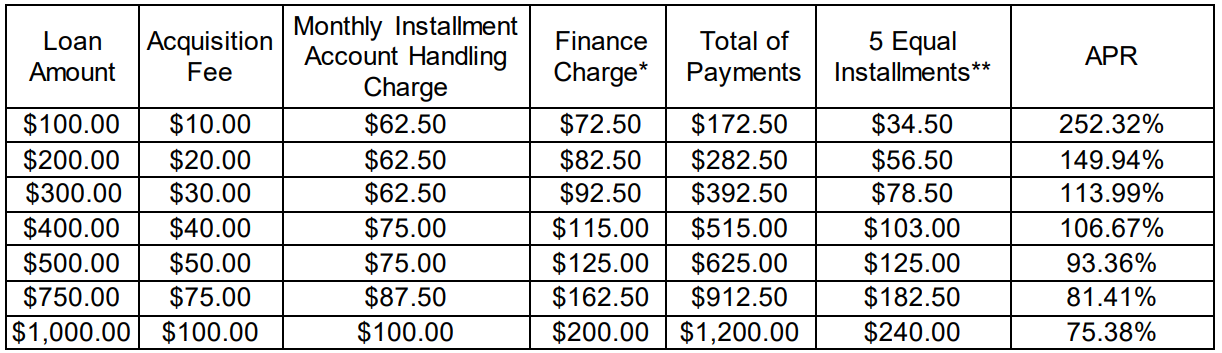

While they don’t currently offer payday loans in Colorado explicitly, they do still have a rates webpage for installment loans in the state, which includes the following terms:

- Amounts from $100 to $1,000 in $10 increments

- Acquisition fees equal to 10% of the loan amount

- Monthly maintenance fees between $12.50 and $20

- A 155-day term, fully amortized in 5 substantially equal payments

Below is a summary of their price points at various standard loan balances.

These terms seem to fly in the face of the Colorado Uniform Consumer Credit Code, and we would recommend taking your business somewhere with an APR below 36% whenever possible.

Most common complaints about Populus Financial Group, Inc.

| Complaint Reason | Count |

| Charged fees or interest I didn’t expect | 5 |

| Can’t contact lender | 4 |

| Received a loan you didn’t apply for | 3 |

| Applied for loan/did not receive money | 1 |

| Can’t stop charges to bank account | 1 |

| Getting the loan | 1 |

| Problem with the payoff process at the end of the loan | 1 |

The most common complaint consumers make about Populus Financial Group, Inc. is that the company charges unexpected fees or interest. Presumably, that happens either because the lender fails to communicate properly, the consumers fail to do their due diligence or both.

While potential borrowers have little to no control over whether lenders correctly disclose their loan details, they can take the following steps to protect themselves from this issue:

- Thoroughly research lenders well before applying for debt, including what other customers have to say

- Closely examine all loan documents before signing; if important information seems to be missing, ask for it

- Do the math on the rates and fees, so there’s no misunderstanding the cost of the loan

Colorado’s payday loan laws are much more restrictive than they were, but lenders may still try to skirt the rules. Consumers must take responsibility for their financial safety because no one else will.

Top 10 most complained about payday lenders

| Lender | No. of complaints since 2013 | Primary complaint reason |

| Populus Financial Group, Inc. | 18 | Charged fees or interest you didn’t expect |

| Wells Fargo & Company | 11 | Charged fees or interest you didn’t expect |

| LDF Holdings, LLC | 8 | Charged fees or interest you didn’t expect |

| GVA Holdings, LLC (out of business) | 7 | Charged fees or interest you didn’t expect |

| Tribal Lending Enterprise, Inc. (no website listed) | 7 | Charged fees or interest you didn’t expect |

| Delbert Services (out of business) | 7 | Charged fees or interest you didn’t expect |

| Synchrony Financial | 6 | Problem when making payments |

| CURO Intermediate Holdings | 6 | Charged fees or interest you didn’t expect |

| BlueChip Financial | 6 | Charged fees or interest you didn’t expect |

| Lending Club Corp. | 6 | Problem when making payments |

Though the industry will hopefully shrink in the future due to the new restrictions, there have been many problematic payday lenders in Colorado over the years.

Even Wells Fargo, one of the nation’s most well-respected banks, is on the list. They have since discontinued the service, but they once offered a $500 deferred deposit advance loan, which was suspiciously similar to a payday loan (with an APR of 120%).

The most complained about tribal lender in Colorado: LDF Holdings, LLC

A notable trend on the list above is the presence of multiple tribal lenders, including LDF Holdings, Tribal Lending Enterprise, and BlueChip Financial. LDF Holdings takes the top spot among them, but the other two are right on its tail with only one or two fewer complaints.

Tribal lenders are predatory companies that partner with a Native American tribe and use their tribal sovereignty to ignore state lending laws. These organizations tend to have even less favorable terms for borrowers than non-tribal payday lenders.

If you’re having financial trouble because of one of these businesses, DebtHammer can help you turn the tables on them. Contact us today for a free quote, and we’ll show you how you can get out of the payday debt trap.

Most common reasons to complain about LDF Holdings

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 4 |

| Received a loan you didn’t apply for | 1 |

| Struggling to pay your loan | 1 |

| Getting the loan | 1 |

| Problem with the payoff process at the end of the loan | 1 |

Payday loan statistics in Colorado

- Colorado ranks as the 25th state for the most overall payday loan complaints.

- Colorado ranks as the 29th state for the most payday loan complaints per capita.

- There have been 18,281 payday loan-related complaints made to the CFPB since 2013 ― 229 of these complaints originated from Colorado.

- The estimated total population in Colorado is 5,758,736 people.

- There are 3.9766 payday loan complaints per 100,000 people in Colorado.

- The second-most popular reason for submitting a payday loan complaint is “Struggling to pay your loan.”

READ MORE: Payday loan debt statistics

Historical timeline of payday loans in Colorado

Like many state lending regulations, the Colorado payday loan laws have gone through different variations over the years. Here’s an overview of the historical timeline:

- Pre-2007 era: Payday loans were common in Colorado, and interest rates regularly reached the mid to high triple digits.

- 2007: Law-makers attempted to reign in unaffordable payday loans. However, they did so while also trying to preserve the business model. Those conflicting goals prevented them from resolving the issue.

- 2010: Learning from their previous failure, regulators introduced a new law that required lower interest rates and longer repayment terms (45% maximum and six-month minimum, respectively).

- 2018: Finally, Proposition 111 passes, which institutes a blanket 36% APR limit for all consumer loans.

The rate cap and repayment-term requirements significantly reduce the financial burden on small-loan borrowers, rendering payday loans effectively illegal.

That said, payday lenders have historically looked for every possible loophole to continue their business model. Consumers in the state should still be wary of debt and do their due diligence to avoid falling into payday loan traps.

Flashback: A Colorado payday loan story

The majority of Colorado’s payday loans stories are rather depressing. Before effective consumer-protection legislation came into effect, you’d see the same song and dance as in every other state that permitted payday loans.

113,694 Colorado payday loans went into default in 2004, representing about 10% of their total payday loans. At the time, loans had an average balance of $317.19 and an average finance charge of $58.33. That works out to an average APR of 380%.

A much more inspiring story is how Colorado came to be a strong example of anti-payday loan laws. Where some states have struggled to sustain their efforts against the notoriously stubborn payday lending industry, Colorado lawmakers made three attempts to curb the industry in a row before eventually reaching their goal.

Not only that, but Proposition 111 (which imposed the 36% APR limit) passed with flying colors. 77.25% of voters supported the bill, which shows an overwhelming amount of support for the cause.

If consumers decide to put their collective feet down and stamp out payday loans across the country, the industry won’t survive.

The bottom line: Should I take out a payday loan in Colorado?

Fortunately, the Colorado payday loan laws effectively prohibit the industry from operating in its traditional form. Deferred deposit transactions must have an APR of 36% or less and a repayment term of six months or more.

You shouldn’t find many traditional short-term, high-interest payday loans in Colorado. If you do, you’re dealing with a lender who is either breaking the law or using some loophole to get around it, like working with a tribe or using an alternative licensing tactic.

Don’t give these lenders your money – take your business elsewhere.

If you need a few hundred dollars of short-term financing, consider using a cash advance app like Earnin or Brigit instead. These have minimal fees and no interest so you won’t fall into a cycle of debt.

Of course, they’re still not a long-term solution for chronic financial shortcomings, so make sure you don’t rely on them too much. If you need these tools to make ends meet because of your current debts, DebtHammer can offer a much more sustainable alternative.

Are you a Colorado resident looking to consolidate your payday loan debt? Contact us for a free quote to start your journey out of debt today!