Payday loans are bad, but tribal payday loans are even worse.

It’s important that before you get any short-term loan, you know whether you’re borrowing from a traditional payday lender or one based on Native American tribal land.

Table of Contents

Everything you need to know about tribal payday loans

If you need an emergency loan, here are some key facts you need to know.

Tribal lenders say they’re exempt from state and federal laws

It’s no secret that payday lenders charge incredibly high fees. However, many state legislatures have started cracking down, passing laws to regulate loan totals and cap interest and fees. In fact, payday loans are now illegal in many states. Tribal lenders argue that these fees don’t apply to them because the U.S. Constitution grants them sovereign immunity (the right to govern themselves). Before you complete an application, it’s important that you research the lender, particularly if you live in a state that strictly caps payday loan interest rates.

Stuck in tribal loan debt?

DebtHammer may be able to help.

Tribal loans are actually installment loans

Payday loans are repaid in a lump sum from your next paycheck. Tribal loans are repaid in installments, often biweekly. This may sound like a positive, because you won’t have to repay your entire loan balance in a lump sum from your next paycheck. However, it means interest will compound, and given the extremely high interest rates, it will compound very quickly.

Many borrowers have reported paying tribal loan companies more than $3,000 to repay an $800 loan.

You will pay a sky-high interest rate

Because of disagreements about regulation, tribal loans are far more expensive than payday loans. The Consumer Financial Protection Bureau (CFPB) says it’s common for payday lenders to charge a $15 fee for a $100 loan. That works out to the equivalent of an almost 400% interest rate for a two-week loan. But tribal lenders charge more. But costs for tribal loans average annual percentage rates, or APRs, between 440% and 1,000% for their installment loans.

Tribal payday loans are downright dangerous

Payday loans are short-term, high-interest loans that you usually repay in a lump sum on your next payday. They’re usually not reported to the credit bureaus and therefore have more relaxed qualification requirements than traditional loans.

Tribal payday loans are largely the same in practice. The only real difference between the two is the lender’s identity (at least on paper). Tribal payday loans are held by payday lenders who claim to operate out of Native American reservations, though the loan companies are almost always entirely online.

That difference might seem harmless at first glance, but it makes tribal payday loans considerably more dangerous. There are virtually no consumer safeguards in place because tribal payday lenders argue that the rules don’t apply.

They aren’t a long-term solution

Many lenders openly state in the terms and conditions that their loans are expensive forms of credit that aren’t suitable for long-term needs.

The loan amounts are usually small

Though some lenders will issue loans up to about $3,000, many cap the loans at about $1,000 or will only loan a small amount to first-time borrowers, who can then borrow more after they’ve successfully repaid the first loan. Some offer “loyalty programs” for repeat customers.

Your lender probably isn’t licensed

Many tribal lenders bypass state licensing regulations. You may see a licensing certificate issued by a particular tribe that looks something like this.

However, that document is not legally binding.

Pro tip: If you can prove that your lender is not appropriately licensed by your state, you may not have to repay your loan.

“It’s illegal to make a loan without a license,” one FTC official told The Center for Public Integrity. “If you’re not licensed, it (the loan) is not collectible and it’s not enforceable.”

If the lender isn’t willing to obtain a license, that should be a red flag that they’re perfectly fine with operating outside the laws,” said Ben Michael, Attorney, Michael & Associates.

You will apply online – the lender won’t have any storefront locations

You don’t need to be a member of a tribal nation to apply. Tribal lenders accept applications online from anyone, regardless of state residency. Try to find a lender that has at least a few storefront locations. That means the lender is licensed by at least one state, and thus won’t be a tribal lender.

Tribal payday lenders can sue you, but they probably won’t

Yes, in theory, a tribal payday loan company can sue you. However, this is typically very rare because there is speculation that suing in state court could jeopardize their sovereign immunity. But they can only sue you if you’ve violated your initial loan agreement and are in default.

Remember tribal lenders can only take you to civil court — not a criminal court — if it even gets to that point. You will not go to jail if you don’t repay your tribal payday loan.

The majority of lenders prefer to negotiate personally. Many will help you create a payment plan rather than settle it in court.

Tribal lenders can garnish wages, but only with a court order

Like every other payday lender, tribal lenders can garnish your wages, but they will have to do it through the court system, and only if all of the following take place:

- You enter into a valid loan transaction with a lender

- You fail to repay the loan balance as you agreed

- The lender sues you and takes you to court

- A judge rules against you in your hearing

If any of the above criteria have not been met, then a tribal lender has no right to garnish your wages.

Though they may make threats, your lender cannot garnish your wages without a court order. In 2014, the Federal Trade Commission reached a settlement with Western Sky Financial and other South Dakota-based tribal payday loan companies that sent letters to employers insisting they had the right to garnish wages without a court order. FTC attorneys say that tribal lenders “do not have the legal authority to garnish the pay of consumers who owe an alleged debt without first obtaining a court order.”

If a lender tries to garnish your wages without a court order, contact an attorney immediately.

READ MORE: Is my payday lender licensed in my state?

The government won’t help (much) with tribal loans

While the federal government has relaxed some rules on repaying certain loans, including student loans and medical debt, the federal government does not offer much help for borrowers stuck with a tribal loan that exceeds state interest rate caps.

The government does not have programs to help you repay your tribal loan, and sovereign immunity limits most regulation efforts.

Your only real option is to prove that your lender is not licensed – many tribal lenders are not. If your lender is not licensed, your loan is illegal. You don’t have to repay illegal loans.

The Consumer Financial Protection Bureau has signaled renewed enforcement of tribal lending.

For example, The Consumer Financial Protection Bureau (CFPB) and FTC have taken various actions against a number of online lenders, including Golden Valley Lending, Inc., Silver Cloud Financial, Inc., Mountain Summit Financial, Inc., Majestic Lake Financial, Harvest Moon Financial, Gentle Breeze Online and Green Stream Lending.

Do some research to find out if there are any pending class-action lawsuits against your lender or tribal lenders as a whole. This could help you qualify for payday loan debt settlement.

There aren’t really any advantages

There is really only one advantage: You can borrow more money than you’d get through a traditional payday lender and the loan doesn’t have to be repaid in a lump sum. Some tribal lenders allow you to borrow as much as $2,000 with no minimum credit score requirement.

There are plenty of disadvantages

Tribal payday loans have the same downsides as traditional payday loans – and then some.

They’re even more expensive than their traditional counterparts, with annual percentage rates (APRs) well into three (or even four) digits.

To put that number into perspective, a standard credit card comes with an APR somewhere between 12% and 36%.

Even worse than their exorbitant prices (which at least you know about ahead of time) is that tribal payday lenders are more likely to practice deceitful or predatory lending tactics than those who are beholden to federal and state law.

Without any need to respect any of the government’s rules or regulations, they’re free to (and often do) surprise borrowers with hidden fees and use any underhanded tactics they like to collect on their loans. And they may change your interest rate without notifying you.

READ MORE: In over your head? 13 ways to escape the payday loan debt trap

The lenders themselves admit the loans are expensive

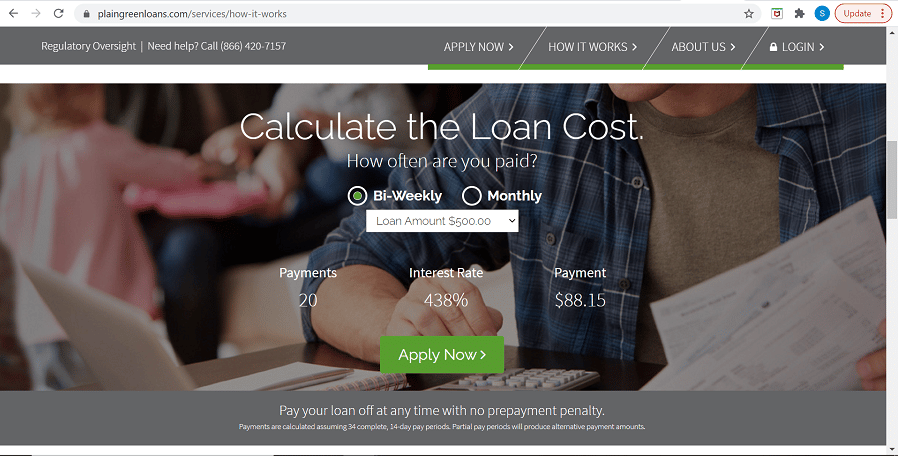

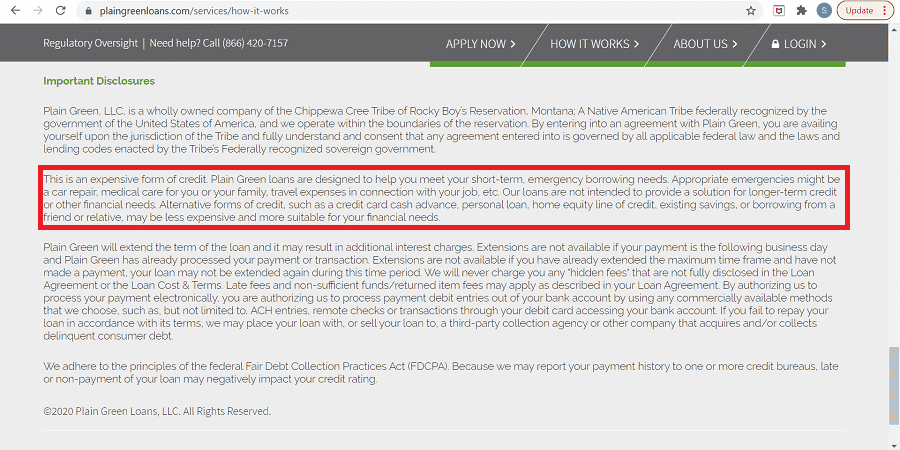

On every tribal lending site, you’ll see a disclaimer that says something akin to the following: “This is an expensive form of borrowing and is not intended to be a long-term financial solution.”

Below you’ll see it under the important disclosures section of Plain Green, LLC. They’re a tribal payday lending company supposedly owned by the “Chippewa Cree Tribe of the Rocky Boy’s Indian Reservation, Montana, a sovereign nation located within the United States of America.”

Plain Green, LLC offers repayment terms between 10 to 26 months, depending on your loan balance. That perfectly demonstrates the danger of tribal payday loans.

Whatever you do, don’t let yourself get sucked into a long-term, high-interest payday loan. Interest always compounds with time, and the results will be disastrous.

READ MORE: 5 easy steps to pay off $10,000 in credit card debt

Ten tribal lenders to avoid

1. SpotLoan

Offering loans up to $800, SpotLoan is owned and operated by The Turtle Mountain Band of Chippewa Indians. SpotLoan sounds like a traditional payday lender until you read the loan terms.

If you borrow $300 and choose to repay it in $58 biweekly installments, you will have to make 21 payments totaling $1,218 to repay your loan in full. That’s more than $900 in interest (an annual percentage rate of 490%).

SpotLoans are only available to residents of Alabama, Alaska, Arizona, California, Colorado, Delaware, Florida, Georgia, Hawaii, Idaho, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Massachusetts, Michigan, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, North Carolina, Ohio, Oklahoma, Oregon, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Washington, Wisconsin and Wyoming.

2. Big Picture Loans

Big Picture Loans is a wholly owned subsidiary of Tribal Economic Development Holdings, LLC, a wholly owned and operated economic arm and instrumentality of the Lac Vieux Desert Band of Lake Superior Chippewa Indians. It offers loans up to $5,000.

Borrowers can expect to pay an APR between 350% to 699%. For context, if you borrow $1,000, you will have to make 26 biweekly payments of about $158. You’d pay more than $3,100 in interest (an APR of 395%).

Big Picture Loans are not available in all 50 states, but no list is provided.

Note: Big Picture Loans is not affiliated with BigPictureLoansUS.com.

3. MaxLend

MaxLend, is wholly-owned and controlled by, the Mandan, Hidatsa, and Arikara Nation. It offers loans up to $3,750. Borrowers can expect to pay an APR between 471% to 841%.

At MaxLend, payments are scheduled for your paydays. This means borrowers who are paid biweekly will make a payment every other week and those who are paid monthly will make a single monthly payment. New customers can only borrow up to $1,000 and typically have nine months to pay back the loan.

If a first-time borrower gets a $1,000 loan repaid in nine months, they will have to make 18 biweekly payments of $190.68. You’d pay more than $2,400 in interest, and that’s if you qualify for the lowest APR of 471%.

MaxLend loans are not available in Arkansas, Connecticut, Georgia, Hawaii, Illinois, Massachusetts, Minnesota, New York, North Dakota, Pennsylvania, Vermont, Virginia, Washington or West Virginia.

4. American Web Loan

American Web Loan is owned and operated by the Otoe-Missouria Tribe of Indians. It offers loans up to $2,500.

American Web Loan does not disclose an APR range on its website or via customer service, but reports indicate that it is between 600% to 780%.

For context, if you borrowed $1,000 repaid over 18 biweekly payments at a 600% APR, you’d repay a total of $4,255 over biweekly payments of $236. The total interest you’d pay is $3,255.

American Web Loan loans are not available in Arkansas, Connecticut, Georgia, Maryland, New York, Vermont and Virginia.

5. Cash Advance Now

GreatPlains Finance, LLC (dba Cash Advance Now) is an entity formed under the laws of the Fort Belknap Indian Community of the Fort Belknap Reservation of Montana. It offers loans up to $1,500 (or $1,200 for first-time borrowers).

If you borrow $500 and repay it biweekly over 10 months, you’ll make 19 payments of $131. You’ll pay a total of $2,489. The total interest you’d pay is $1,989 and the APR is 700%.

Cash Advance Now does not issue loans in all 50 states, but it does not provide a list of where the loans are available.

6. Target Cash Now

Target Finance, LLC (dba Target Cash Now) is an entity formed under the laws of the Fort Belknap Indian Community. First-time customers can borrow up to $2,000, while repeat customers can borrow up to $2,500.

If you borrow $400, you will have to make 12 biweekly payments of $127.50 for a total of $1,529.96, including $1,129 in interest and an APR of 795%.

Target Cash Now does not lend to residents of Arkansas, Connecticut, Minnesota, Montana, New Jersey, New York, Pennsylvania, Virginia and West Virginia.

7. Greenarrow Loans

Green Arrow Solutions is wholly owned and operated by the Big Valley Band of Pomo Indians. It offers loans up to $1,500 (or $300 for first-time borrowers).

Greenarrow doesn’t disclose the interest rates it charges, but a sample loan indicates an APR of 825%. In the example, a $300 loan is repaid in nine biweekly payments of $101.68. You’ll pay more than double the amount you borrowed in interest alone.

Greenarrow Loans are not available in Arkansas, Colorado, Connecticut, Georgia, Illinois, Maryland, Minnesota, Montana, New Hampshire, New York, North Carolina, Pennsylvania, Puerto Rico, Vermont, Virginia, Washington and West Virginia.

8. Uprova

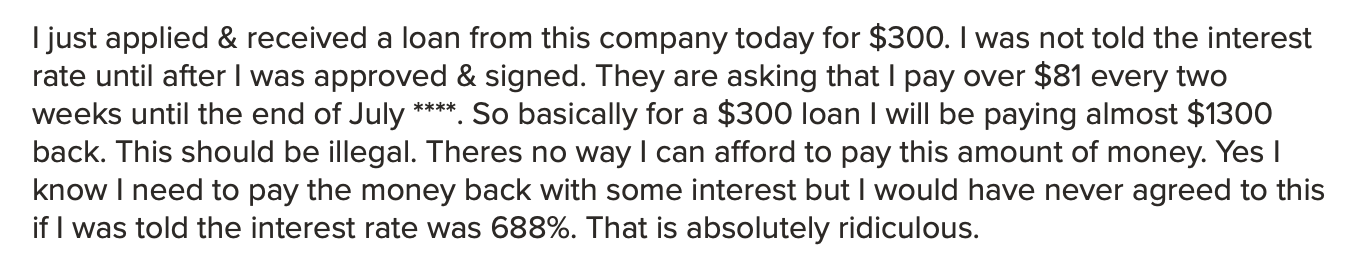

Uprova Credit, LLC. is a tribal lending entity wholly owned and operated by the Habematolel Pomo of Upper Lake, California. It offers loans up to $5,000.

Uprova’s website says “APRs can range from 34.5% to 35.99%.” However, customer reviews indicate that interest rates are significantly higher.

For example, this complaint was posted on Uprova’s Better Business Bureau page, which also spells out how much borrowers should expect to pay for an Uprova loan:

Buried in the fine print is a notice that states: Short term loans at higher APRs are available for other customers.”

Currently, you can only borrow through Uprova if you live in the following states: Alaska, Arkansas, California, Delaware, Florida, Hawaii, Idaho, Iowa, Kansas, Louisiana, Maine, Michigan, Mississippi, Missouri, Nebraska, Nevada, New Hampshire, North Dakota, Oklahoma, Oregon, Rhode Island, South Carolina, Tennessee, Texas, Utah, Washington, Wisconsin and Wyoming. Residents of other states will be referred to Uprova’s affiliate, Mountain Summit Financial.

9. Blue Mountain Loans

Blue Mountain Loans is a brand of Loan Spot, a wholly owned subsidiary of Kashia Services, a wholly owned economic arm and instrumentality of the Kashia Band of Pomo Indians of the Stewarts Point Rancheria. It offers loans between $100 and $1,200.

Blue Mountain Loans does not disclose it’s interest rate range, but the website states “Our interest rates are competitive and in accordance with Tribal and federal laws. The loans have a maximum APR of 660% but you may qualifier for a lower rate based on your credit history or prior performance.”

Repayment schedules are based around your pay schedule: You’ll make weekly payments if you’re paid weekly, bi-weekly payments if you’re paid every two weeks and monthly if you’re paid once a month.

If you borrow $300 repaid biweekly over 10 payments at 660%, you’ll repay $850.05 in payments of $85.01.

Residents of Arkansas, Connecticut, Massachusetts, Maryland, New York, Pennsylvania, Vermont, Virginia and West Virginia are not eligible for Blue Mountain Loans.

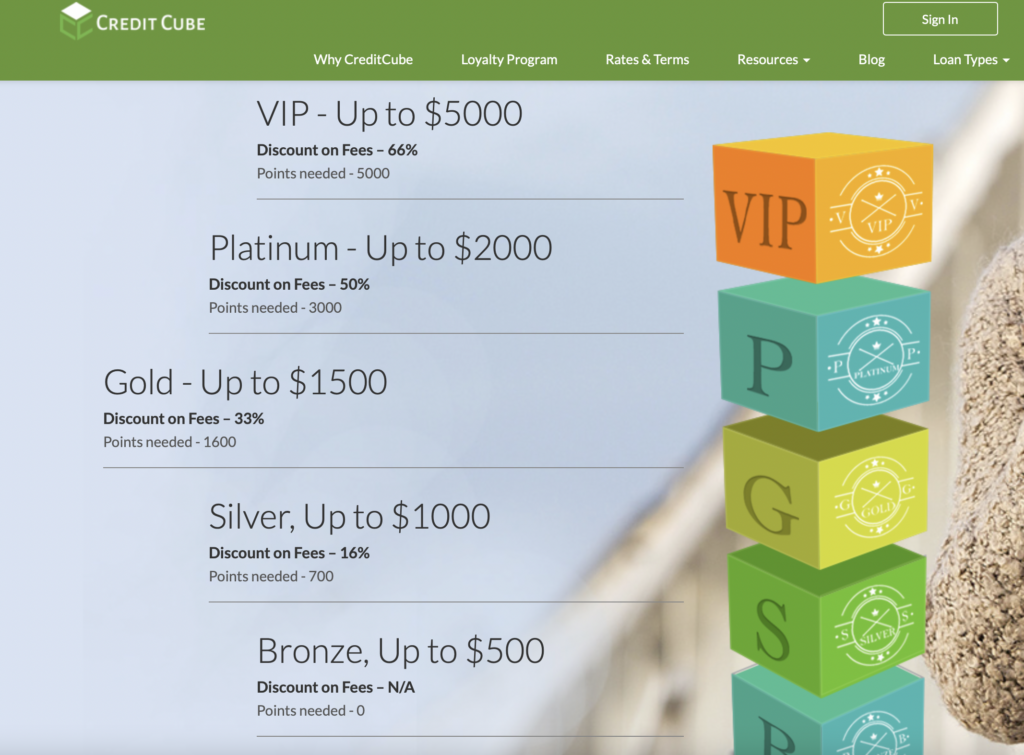

10. CreditCube

CreditCube is owned and operated by the Big Valley Band of Pomo Indians. It offers installment loans up to $5,000, but the maximum loan amount for first-time borrowers is $500.

Credit Cube’s interest rates range from 259.94% (for repeat borrowers) to 779% for first-timers.

Here is a comparison of a $300 loan repaid in 16 biweekly payments for new customers vs. the same loan for “VIPs.”

CreditCube does not lend to residents of Pennsylvania, Connecticut, Minnesota, New York, Vermont, Virginia, West Virginia and Georgia.

You have better options

If you have bad credit, you may believe these loans are your only option. That’s no longer the case. Cash advance apps and peer-to-peer lending platforms will usually consider borrowers with bad credit. Even Reddit offers a subreddit called r/borrow where fellow Redditors will consider lending you money.

Many of the strategies that are effective at escaping the traditional payday loan cycle would work for getting out of the tribal payday loan trap as well.

For example, here are some other great alternatives:

READ MORE: 10 Best Cash Advance Apps for Instant Money

Break the tribal payday loan cycle

If you’re struggling to find your way out of the tribal payday loan trap by yourself, consider getting expert help. DebtHammer specializes in helping borrowers like yourself escape both the traditional and the tribal payday loan traps. Contact us today for a free consultation, and we’ll get you started right away.

READ MORE: Payday loan consolidation and debt relief that works

The bottom line

No matter how desperate you are, tribal payday loans will almost certainly make your financial situation even worse. Carefully research all lenders to ensure that you don’t get trapped with a loan that will end up costing you three times the initial amount you borrowed.