Payday loans are short-term loans with no credit check that unqualified borrowers can use in emergencies. However, they’re highly controversial since their high finance charges often create more problems for borrowers than they solve. As a result, each state regulates them differently. Here’s how the New Jersey payday loan laws work.

Table of Contents

Payday lending status in New Jersey: Prohibited

Fortunately, New Jersey regulators have prohibited the payday lending industry. In addition to a criminal usury rate cap of 30% on consumer loans, there’s also a law forbidding anyone from making cash advances on post-dated checks.

Both restrictions target payday loans, which traditionally carry interest rates well into the triple digits and usually require borrowers to secure their loans with a post-dated check for the loan amount and finance charge.

You can read the full text of the relevant regulations in the New Jersey Revised Statutes under Title 2C: 21-19: Wrongful Credit Practices and Related Offenses and Title 17: 15A-47: Prohibitions for Licensees.

READ MORE: States where payday loans are illegal

Stuck in payday debt?

If you’re a New Jersey resident, DebtHammer may be able to help.

Loan terms and debt limits in New Jersey

Maximum Interest Rate: 30%

Payday loans are short-term, high-interest loans that you can qualify for even with bad credit. Allegedly, they’re supposed to support people during financial emergencies when they can’t get other forms of financing.

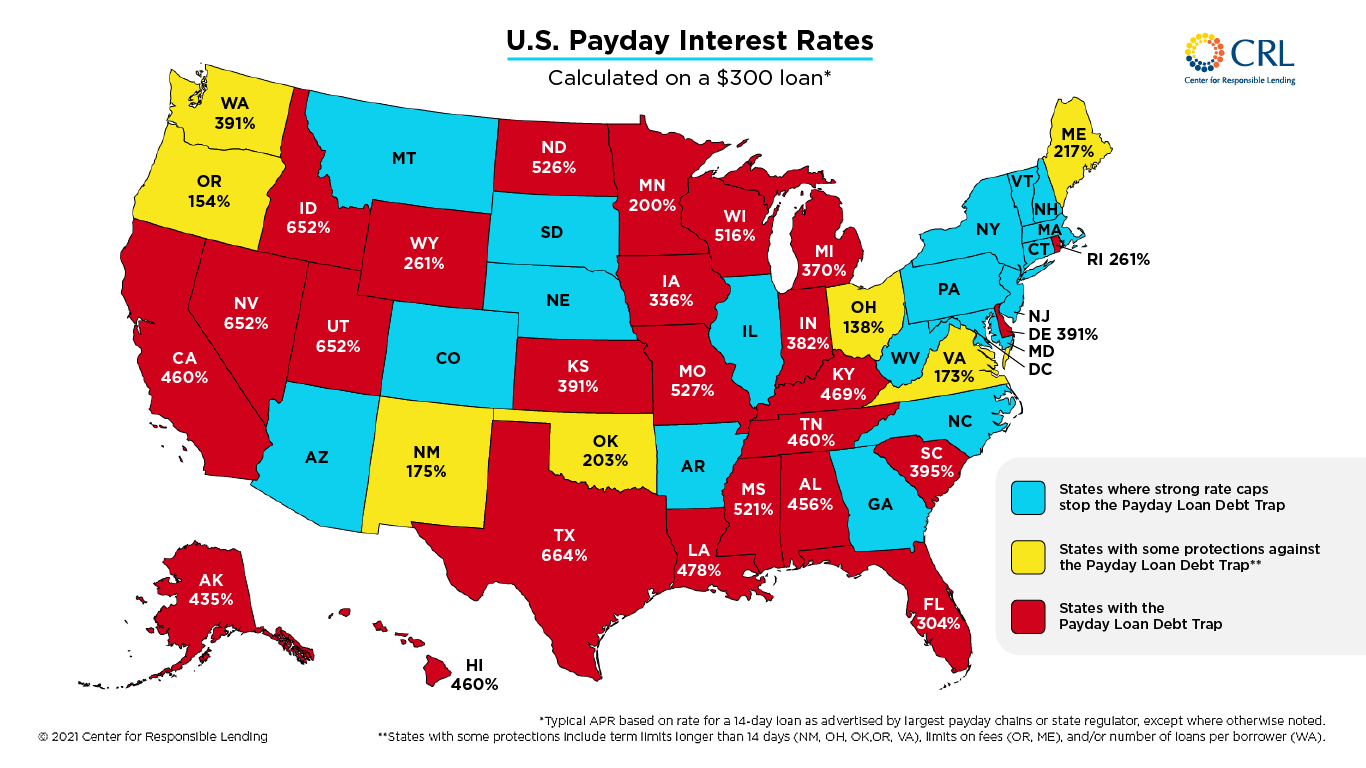

However, typical payday loan costs are so high that borrowers often have trouble paying back their debts. For example, the average payday loan in Texas has a 664% annual percentage rate (APR).

{kind=link}

When borrowers can’t afford their payday loans, they often pay a rollover fee to extend the due date or take out another loan to pay off the original. Either way, they get stuck in a cycle of debt that’s hard to escape.

The most effective way to prevent that trap is to cap interest rates at reasonable levels. In New Jersey, the 30% usury limit is well within an affordable range for most consumers, making the traditional payday lending trap illegal.

READ MORE: Guide to debt relief in New Jersey

New Jersey payday loan laws: How they stack up

The New Jersey payday loan laws are much more restrictive than the regulations in most other parts of the country.

They’re one of only 21 states that have banned the practice outright via reasonable rate caps. They’re unusually pro-consumer even among their fellows since the typical usury limit is 36% APR.

Here’s a more detailed explanation of the New Jersey regulations to help you understand how they stack up against other state lending laws.

READ MORE: How to get out of payday loan debt

Rates, fees, and other charge limits in New Jersey

The state of New Jersey includes two separate sets of usury limits: civil and criminal. The civil usury limit caps consumer loans without a contract at 6% interest per year, while those with a written agreement can bear up to 16% annually.

Unfortunately, the civil usury limit is often irrelevant due to the many exceptions to the rule. For example, revolving credit accounts, installment loans, and financing from traditional financial institutions are all exempt.

However, the criminal usury limits are much more robust. They prevent lenders from charging more than 50% for loans to corporations, limited liability companies, and limited liability partnerships or more than 30% for loans to anyone else.

READ MORE: Payday loan consolidation and relief that works

Are tribal loans legal in New Jersey?

The federal government considers Native American tribes sovereign nations within the United States. As a result, they have the right to govern themselves, which means they’re generally immune to lawsuits for breaking state law.

Tribal lenders partner with Native American tribes to share their immunity and use it to charge interest rates higher than state regulations allow. In exchange, they offer the tribe a small portion of their profits.

Unfortunately, tribal lenders exist in something of a legal gray area. It’s difficult for regulators to impose restrictions on them due to their tribal immunity and the fact they operate exclusively online.

However, their loan agreements are generally unenforceable in state courts, including New Jersey’s. You need specific lending licenses to operate in each state, and tribal lenders never have them. As a result, they can’t sue you in a court that has any authority to garnish your wages or force you to pay.

READ MORE: Is my payday loan lender licensed?

Consumer information

The New Jersey Department of Banking & Insurance is the agency in charge of overseeing financial institutions in the state. More specifically, their Division of Banking has an Office of Consumer Finance that regulates financial services for consumers.

That primarily means enforcing the statutes that protect consumers against predatory lenders. They respond to consumer inquiries and investigate their complaints about state-chartered financial institutions and the rest of the Division of Banking’s licensees.

READ MORE: How to get out of high-interest tribal loans

Where to make a complaint

The New Jersey Department of Banking & Insurance is the best place to submit a complaint about a payday lender. More specifically, you can report them to the Division of Banking, which houses the Office of Consumer Finance. Here’s how to contact them.

- Regulator: Department of Banking & Insurance, Division of Banking

- Physical Address: 20 W State St, Trenton, NJ 08625

- Mailing Address: NJDOBI, PO Box 471, Trenton, NJ 08625-0471

- Phone number: 609-292-7272 or 1-800-446-7467

- Website: https://www.state.nj.us/dobi/consumer.htm

It’s also good to send your complaint to the Consumer Financial Protection Bureau (CFPB). The CFPB is a federal agency that protects consumers from predatory financial institutions, including payday lenders.

Number of New Jersey consumer complaints by issue

These statistics are all according to the CFPB Consumer Complaint Database.

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 227 |

| Struggling to pay your loan | 39 |

| Can’t contact lender or servicer | 33 |

| Problem when making payments | 31 |

| Getting the loan | 28 |

| Problem with the payoff process at the end of the loan | 23 |

| Received a loan you didn’t apply for | 19 |

| Can’t stop withdrawals from your bank account | 15 |

| Incorrect information on your report | 12 |

| Loan payment wasn’t credited to your account | 10 |

| Applied for loan/did not receive money | 9 |

| Money was taken from your bank account on the wrong day or for the wrong amount | 8 |

| Problem with additional add-on products or services | 5 |

| Vehicle was damaged or destroyed the vehicle | 5 |

| Vehicle was repossessed or sold the vehicle | 2 |

| Was approved for a loan, but didn’t receive money | 2 |

| Problem with a credit reporting company’s investigation into an existing problem | 2 |

| Improper use of your report | 2 |

Source: CFPB website

The most common complaint individuals send to the CFBP in New Jersey is that their lenders have charged them fees or interest that they didn’t expect. That’s true in many parts of the United States, but it’s especially true in New Jersey, where there are six times as many instances as the next most common issue.

Many factors contribute to this problem, including that borrowers don’t always perform the necessary due diligence and that lenders sometimes inadequately disclose their loan costs.

In addition, New Jersey consumers might have a false sense of security since they have a usury rate limit of 30%. Unfortunately, the predatory businesses that engage in practices like payday lending are often willing to exploit loopholes and demand fees beyond that cap.

The most complained about lender in New Jersey: Delbert Services

The most commonly complained about lender in New Jersey is Delbert Services, though they’re not a lender per se. Delbert Services was a debt collection agency previously associated with CashCall, a predatory tribal lender.

CashCall couldn’t take borrowers to court due to its tribal status, but Delbert Services was a licensed debt collector. They worked together to fill in the holes in each other’s operations, charging excessive interest rates through the tribal entity and then collecting the debts through the licensed one.

Fortunately, neither Delbert Services nor CashCall is in business anymore. Multiple regulators targeted their operation, ordering them to cease issuing and collecting on loans that violate state laws, including the CFPB and the Massachusetts Office of Consumer Affairs and Business Regulation.

Most common complaints about Delbert Services

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 38 |

| Can’t stop withdrawals from your bank account | 1 |

| Can’t contact lender or servicer | 1 |

Source: CFPB website

The most common reason consumers complained about Delbert Services was that they charged fees or interest that borrowers didn’t expect. Since they were essentially an extension of CashCall, which was charging people in New Jersey far more than what was legal in the state, that shouldn’t surprise you.

Top 10 most complained about payday lenders

| Lender | Number of Complaints Since 2013 |

| Delbert Services | 40 |

| BlueChip Financial | 31 |

| LDF Holdings, LLC | 30 |

| GVA Holdings, LLC | 20 |

| Mobiloans, LLC | 18 |

| Tribal Lending Enterprise, Inc. | 16 |

| MoneyLion Inc. | 15 |

| Wells Fargo & Company | 13 |

| Kashia Services | 12 |

| CashCall, INC. | 12 |

Source: CFPB website

Delbert Services is the most complained about lender in New Jersey, but not by a very significant margin. Several other businesses in the state have inspired almost as many people to reach out to the CFPB.

Notably, most of them are tribal lenders. In fact, seven out of the top ten most complained about lenders in the state are tribal. BlueChip Financial, LDF Holdings, GVA Holdings, Mobiloans, Tribal Lending Enterprise, Kashia Services, and CashCall are all extensions of Native American tribes.

Unfortunately, that means the 30% usury rate cap doesn’t protect borrowers in New Jersey from predatory lenders as well as it should. Governmental protections against payday loans can only do so much. Plenty of lenders are willing to subvert the law and continue to charge triple-digit interest rates.

As a result, you must still do your due diligence before taking out a loan in the state. Check each lender’s license to practice, thoroughly review their loan terms, and confirm that you can afford to pay the prospective obligations before signing.

If you’re facing financial difficulties because of the lenders on the list above or others like them, then contact DebtHammer today. We’ll help you get out of the debt trap once and for all.

The Most Complained About Tribal Lender in New Jersey: BlueChip Financial

Delbert Services is the most complained about lender in New Jersey, but BlueChip Financial is only slightly behind. There have only been nine more complaints about Delbert than BlueChip since 2013. That also makes them the most complained about tribal lender in the state.

BlueChip Financial does business through their subsidiary Spotloan, through which they offer short-term installment loans to people with bad credit in emergencies, much like traditional payday lenders. Here’s what they offer:

- 490% maximum APR

- 10-month maximum repayment term

- Principal balances between $300 and $800

As you can see, their interest rates far exceed the 30% usury rate cap in New Jersey, thanks to their tribal immunity. They can be even more expensive than typical payday loans due to their longer repayment terms. For example, if you borrow $600 at 490% and pay back the amount over five months, you’d incur $775 in finance charges.

Most Common Complaints About BlueChip Financial

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 16 |

| Struggling to pay your loan | 4 |

| Money was taken from your bank account on the wrong day or for the wrong amount | 3 |

| Received a loan you didn’t apply for | 3 |

| Can’t contact lender or servicer | 3 |

| Problem with the payoff process at the end of the loan | 2 |

Source: CFPB website

As you can probably guess, the most common reason people complain to the CFPB about BlueChip Financial is that they charge unexpected fees or interest. That makes a lot of sense since their interest rates can be as high as 490%, and everything above 30% is supposed to be illegal.

Payday loan statistics in New Jersey

- New Jersey ranks as the 10th state for the most overall payday loan complaints.

- New Jersey ranks as the 18th state for the most payday loan complaints per capita.

- There have been 18,281 payday loan-related complaints made to the CFPB since 2013 ― 472 of these complaints originated from New Jersey.

- The estimated total population in New Jersey is 8,882,190 people.

- There are 5.3140 payday loan complaints per 100,000 people in New Jersey.

- The most popular reason for submitting a payday loan complaint is “Charged fees or interest you didn’t expect.”

READ MORE: Payday loan debt statistics

Historical timeline of payday loans in New Jersey

Fortunately, the New Jersey payday loan laws have included hard usury rate caps for many years. As a result, there hasn’t been much need for significant changes to the local payday lending regulations.

In fact, the only two significant highlights to be aware of are the following:

- 1979: The New Jersey Code of Criminal Justice was established, which codified the 30% criminal usury rate that prevents payday lenders from charging their excessive fees.

- 1993: The Check Cashers Regulatory Act passed, preventing them from offering advances on post-dated checks, which is the typical strategy that payday lenders employ.

Because these are such strict lending laws for licensees in New Jersey, it’s always in your best interest to work with legitimately licensed businesses. Otherwise, you risk dealing with entities that disregard state lending laws, such as tribal lenders.

You can look up licensees to confirm their status on the New Jersey Division of Banking and Insurance’s website.

Flashback: An New Jersey payday loan story

Unfortunately, consumers and financial service providers often have a direct conflict of interest. In many cases, the institutions profit by taking as much money from their clients as possible. Lenders are perhaps the most obvious example since their bottom line correlates directly with their ability to charge you higher finance fees.

As a consumer, that means you can’t trust financial institutions to look out for your best interest. In fact, there’s no guarantee that they’ll even follow the law. As a result, you must take responsibility for your finances and do the necessary due diligence before doing anything that could leave you vulnerable.

For example, consider the story of Angel Gordon, a New Jersey resident who took out an illegal payday loan from an online lender in 2013. She borrowed $800 from National Opportunities Unlimited, Inc.

It took her ten weeks to repay the balance, and she ended up incurring roughly $1,000 in finance fees during that period. Those charges blatantly exceeded the 30% criminal interest rate cap in New Jersey.

Unfortunately, National Opportunities Unlimited wasn’t the only one skirting the law in that transaction. U.S. Bank allegedly originated the transactions for the payday lender, facilitating the electronic transfers that removed Gordon’s funds from her bank account, despite knowing that the loans were illegal and usurious.

Gordon complained to the CFPB and started a class-action lawsuit against the financial institutions. Her lawyer, former Kansas Attorney General Steve Six stated: “Without U.S. Bank aiding these payday lenders in processing the illegal loans, they would not be able to prey on consumers like Angel.”

The bottom line: Should you take out a payday loan in New Jersey?

Roughly 48% of American adults would struggle or be entirely unable to pay a sudden $400 expense. If you don’t have the cash for an emergency like that and happen to have bad credit, payday loans can seem like the only way to pay your bill.

However, they almost always cost so much that they make situations worse after only a brief reprieve. New Jersey prohibits payday loans, so the only ones available come from organizations willing to break the rules, like tribal lenders. And as you know, their products are even more dangerous to consumers.

As a result, you should always do your best to avoid taking out payday loans in New Jersey. Fortunately, there are more viable alternatives than you might think, even with poor credit. For example, you could use a cash advance app like Dave, which lets you borrow against your wages with no interest or fees.

These short-term solutions can give you some much-needed breathing room without creating an even bigger problem a few weeks later. However, they won’t be able to sustain you forever. Eventually, you’ll need to save an emergency fund so that you don’t need to go into debt for surprise expenses.

If you want help with that process so you can make predatory lenders a thing of your past, contact DebtHammer today!