It’s no secret that payday loans can hurt your financial situation. But how do payday loans affect your credit score?

Table of Contents

Our take

- Payday loans almost never help your credit score, but late payments can seriously hurt your credit score

- Payday lenders don’t report payday loans to the three major credit bureaus

- Payday lenders have their own credit reporting services, so keep in mind that if you default on a payday loan, other payday lenders will know

- If you don’t repay your payday loan and it’s turned over to debt collectors, it will seriously hurt your credit score

- If you can’t repay your payday loan on time, don’t default — contact your creditor and ask for an extension or extended payment plan

- An unpaid payday loan will stay on your credit report for seven years

READ MORE: Simple steps to get out of payday loan debt

Stuck in payday debt?

DebtHammer may be able to help.

Payday loans won’t help your credit score – they can only hurt it

Typically, payday loans only impact your score when you don’t pay them back by the due date. Unfortunately, this is far more likely to happen with payday loans than most other types of loans.

Payday loans typically don’t appear on credit reports from the major credit bureaus (TransUnion, Experian and Equifax) as long as you repay the loan as scheduled. This means that they will not affect your credit score. This is both good and bad: Your score won’t decrease, but the loans won’t help you build credit.

Payday lenders have their own credit reporting agencies that are only used by payday lenders. These include FactorTrust and Clarity. This means that other payday lenders will know if you default on one payday loan, and that will make it difficult for you to get another loan.

Timely payments aren’t reported to the major credit bureaus

Payday loans are the worst of both worlds: You won’t receive any reward for good behavior or responsible use, but you’ll definitely receive punishment for defaulting.

Since payday loan providers won’t report your good behavior, you usually can’t use them to rebuild bad credit. They keep your repayments a secret … until you stop making them.

Unfortunately, if you don’t repay a payday loan, it may be charged off or sent to collections, negatively affecting your credit score.

Pro tip: Since most payday loan borrowers already have a thin credit file or poor credit, this means payday loans have almost no advantages over other types of loans, including Payday Alternative Loans.

READ MORE: What happens when you default on a payday loan?

How payday loans hurt your credit score

When you fail to pay back your payday loan (which studies have shown as many as half of borrowers eventually do), your lender has a few ways of trying to collect. And unfortunately, almost all of them will cause your credit score to drop.

These include:

- Debt collectors: If your payday lender decides to sell your loan to a debt collector, the collector will be under no obligation to keep your default a secret from the credit bureaus.

- Lawsuits: Your payday lender has the right to sue you when you breach the terms of your payday loan. If you’re taken to court and ruled against (either because you’re guilty or simply fail to show up), it will be reported to a credit bureau and damage your credit score.

READ MORE: How long do payday loans stay in the system?

To top it off, an account in collections and a lost lawsuit negatively impact your “payment history,” which is another key factor used to calculate your credit score.

READ MORE: How to find out if you have outstanding payday loans

What credit score is needed for a payday loan?

Most payday lenders don’t run credit checks at all, so there is no minimum credit score requirement for payday loans. The loan application process is simple and qualifications are minimal. All you need is an ID, proof of income, a bank account and to be age 18 or up.

READ MORE: Payday loan requirements

How credit scores are calculated

Before you can fully understand how much your payday loan could affect your credit score, you need to know how lenders calculate your credit score in the first place.

There are three primary credit scoring models: FICO, VantageScore 3.0 and VantageScore 4.0. As you can see, they use slightly different criteria to calculate your credit score.

| FICO | VantageScore 3.0 | VantageScore 4.0 |

| 35% payment history | 40% payment history | 41% payment history |

| 30% amounts owed | 21% depth of credit | 20% depth of credit |

| 15% length of credit history | 20% credit utilization | 20% credit utilization |

| 10% new credit | 11% balances | 6% balances |

| 10% credit mix | 5% recent credit | 11% recent credit |

| 3% available credit | 2% available credit |

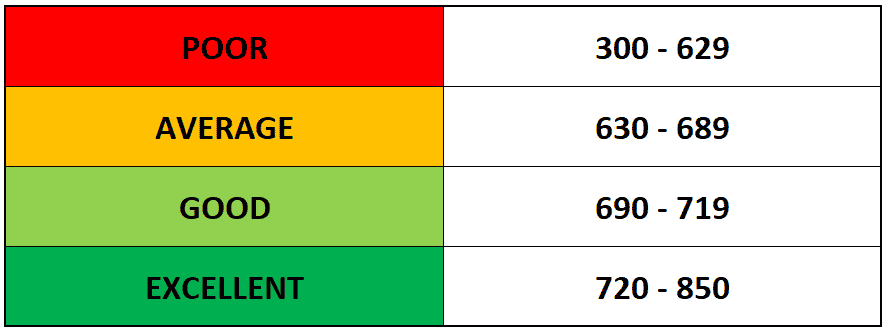

Lenders apply their preferred formula to the details in one or more of your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion. The resulting score is an approximate representation on a scale of 300 to 850 of how risky it would be for them to lend to you.

READ MORE: Five easy steps to pay off $10,000 in credit card debt

How to avoid credit score damage from payday loans

It’s difficult to take out payday loans without getting burned eventually, but it is theoretically possible. If you use them responsibly and intelligently, you might be able to avoid damaging your credit score.

Pay your loan by the due date

You’ll need to ensure you can repay your loan on time and in full. If you ever default on a payday loan, you’ll see a significant hit to your credit score.

READ MORE: Are payday loans secured or unsecured loans?

Ask for an extended payment plan

If you can’t repay your loan as scheduled, the best way to protect your credit score is to talk with your lender.

Most lenders in states where payday loans are legal must offer no-cost extended payment plans. Still, research from the Consumer Financial Protection Bureau (CFPB) shows that borrowers are not taking advantage of this option and instead continue to pay for expensive loan rollovers.

“Our research suggests that state laws that require payday lenders to offer no-cost extended repayment plans are not working as intended,” said CFPB Director Rohit Chopra in a news release. “Payday lenders have a powerful incentive to protect their revenue by steering borrowers into costly re-borrowing.”

READ MORE: All about payday loan extended payment plans (EPP loans)

Payday loans are difficult to repay

Payday loans are short-term loans with extremely high interest rates. Because they’re designed to be repaid from your next paycheck, the tight turnaround makes it virtually impossible for them to be repaid on time, even though the loan amounts are usually small. This often forces borrowers to roll them over into new, even more expensive loans. It can lead to borrowers trying to get a second payday loan at once or eventually causing borrowers to default.

The application process is designed to target borrowers who already have bad credit. Eligibility is simple. You only need a bank account, proof of income and an ID. So, payday loan borrowers usually live paycheck to paycheck and have limited borrowing options.

READ MORE: Payday loan interest rates

How to remove payday loans from your credit report

If one or more payday loans end up on your credit report and are damaging your credit score, it will take a lot of time, effort, or both to have them removed.

That said, there are a few ways to fix your credit or have a payday loan (or any other debt) taken off your credit report.

The most common ways are:

- Dispute an error: If you think a payday loan has been mistakenly entered on your credit report, you can write to a credit bureau and request that the error be investigated and removed. If you find a clerical error or have been the victim of identity theft, this is the best way to take a payday loan off your credit report.

- Negotiate with your lender: If the loan you’re trying to remove isn’t due to a mistake, it will be much more challenging to get it taken off. In this case, negotiate with the reporting lender or debt collection agency. If you offer to pay the old debt in full, they might be willing to remove the negative entry from your report.

- Goodwill requests: Since you defaulted on the debt, you probably don’t have the money to pay it off. If you can’t make payments on the loan you wish to have removed from your credit report, it’s still worth asking the lender to remove it. The worst they can say is no, and they might be lenient.

If none of these strategies work, you may simply have to wait out the problem. It’s not ideal since the damage can limit your credit options, but the loan will be removed from your report after seven years.

In the meantime, focus on improving the other components of your credit score (you can even set up a free consultation with a credit counselor) and as time passes, the damage from the payday loan will lose some significance.

READ MORE: How to increase your credit score

Better options to break the payday loan debt cycle

- Payday loan consolidation programs

- Cash advance apps

- Personal loans

- Credit counseling

- Credit union loans

- Debt consolidation loans

- Credit card balance transfers

READ MORE: Payday loan alternatives

The bottom line

Make your payments on time, every time. Try to avoid taking out any more payday loans since those are so difficult to repay and are what got you in trouble in the first place. In fact, more than 90% of payday loan borrowers regret their payday loan.

If you’re struggling to keep up with your payday loans, DebtHammer can help. We specialize in helping people escape the payday loan trap, so if you’re looking to avoid defaulting and damaging your credit score, contact us today.