Payday loans are a short-term, high-interest form of credit that often traps borrowers in a vicious cycle of debt. They’re a controversial topic in America, and because state governments regulate them independently of each other, each one follows a unique ruleset. Here’s what you should know about the Texas payday loan laws if you live in the state.

Table of Contents

Payday lending status in Texas: Legal

The Texas payday loan laws are simultaneously among the most complex and the least restrictive in the country. There are a total of four sections that regulate entities with various potential payday lending licenses within the state, including:

- Tex. Fin. Code Ann. §341

- Tex. Fin. Code Ann. §342

- Fin. Code Ann. §393

- 7 Tex. Admin. Code §83, Subchapter B

Unfortunately, these limitations are only as strong as their weakest link. In this case, that weak link is Tex. Fin. Code Ann. §393.

It lets payday lenders claim a license as a credit access business. A credit access business serves as an intermediary between consumers and third-party lenders. In Texas, there are virtually no limitations at the state level on the fees they can charge.

The relevant section of the statute states the following: “Nothing in [this section] grants authority to the finance commission or the Office of Consumer Credit Commissioner to establish a limit on the fees charged by a credit access business.”

READ MORE: States where payday loans are illegal

Stuck in payday debt?

If you’re a Texas resident, DebtHammer may be able to help.

Loan terms, debt limits, and collection limits in Texas

- Maximum loan amount: N/A

- Maximum Interest Rate (APR): N/A, due to the credit access business loophole

- Minimum loan term: 7 days

- Maximum loan term: 180 days

- Number of rollovers allowed: Any

- Number of outstanding loans allowed: Any

- Cooling-off period: None

- Finance charges: Any, due to the credit access business loophole

- Criminal action: No, except in case of forgery, fraud, or theft

Payday loans have incredibly high interest rates and short repayment terms, making it highly unlikely that borrowers will have the money to afford their payments when they come due.

Payday lenders then trap them in a cycle of debt by charging them a series of rollover fees that continually reset the life of the loan. Unfortunately, the Texas payday loan laws do nothing to prevent credit access businesses from abusing consumers like this.

READ MORE: Guide to debt relief in Texas

Texas payday loan laws: How they stack up

When it comes to payday loans, Texas is a unique case. Its state government lets payday lenders slip through gaping regulatory holes and continue to charge consumers excessive fees without restriction.

However, city and local governments in the state have taken it upon themselves to begin cracking down on the industry. Many areas have adopted additional credit access business regulations of their own volition. Fortunately, they all follow a virtually identical template.

However, two Texas cities still ended up on our list of top 10 cities with the worst payday lending problems.

Let’s take a closer look at the payday loan limitations in Texas for areas with and without the additional regulations.

READ MORE: How to get out of a payday loan nightmare

Maximum loan amount in Texas

There is no specified maximum loan amount for payday loans issued through the credit access business loophole. In areas without any additional local protections, payday lenders can offer loans for however much they like, though they’ll still tend to top out at $500 to $1,000 since that’s what consumers demand.

However, in areas that have implemented the additional local regulation template, a credit access business can’t provide a deferred presentment transaction, or payday loan, that exceeds 20% of the consumer’s gross monthly income.

For example, say you make $3,000 a month before taxes. A payday lender could not use the consumer access business loophole to give you a loan for more than $600.

READ MORE: Payday loan consolidation and relief that works

What is the statute of limitations on a payday loan in Texas?

The statute of limitations refers to the period that a debt collector can initiate a lawsuit to collect on your outstanding debts. After it expires, there’s no point in pursuing legal measures because a court can no longer order you to pay the balance.

In Texas, the statute of limitations on debt is four years.

Rates, fees, and other charge limits in Texas

In the areas of Texas where there is no local regulation to prevent payday lenders from taking advantage of the credit access business loophole, they can charge just about whatever they can convince a consumer to pay.

In areas that have implemented the standard local regulations, there are no rate limits per se, but there is a rollover clause that prevents borrowers from getting trapped in a cycle of endless debt.

Any payday loan that consumers must pay back in a single lump sum can have no more than three rollovers, and at least 25% of the proceeds from each rollover must go toward the principal amount of the loan. Any loan issued within seven days of a previous loan’s payoff counts as a rollover.

Maximum term for a payday loan in Texas

Payday loans from credit access businesses have a maximum term limit of 180 days in Texas. They can also have repayment terms as short as seven days.

Likely because there is already a state-mandated maximum term for loans from credit access businesses, the local ordinance template does not include a term limit.

Consumer information

The Texas Office of Consumer Credit Commissioner licenses and regulates non-depository lenders that offer loans to consumers in the state. Payday lenders with a credit access business license fall under their jurisdiction.

The office helps resolve issues that consumers have with regulated lenders. Their mission is to protect consumers and creditors under their purview respond to complaints correctly. When necessary, they may serve as a mediator for disputes.

How many payday loans can you have in Texas?

No law limits the number of payday loans Texans can have simultaneously, but if you need more than one, you’ll likely have to use a different lender. Though payday lenders don’t report loans to the three major credit bureaus, they do have their own reporting system, so if you already have a couple of outstanding payday loans — or have defaulted on a previous payday loan — the new lender will typically be aware.

There’s also no overall limit to the number of payday loans Texans can have, so once you pay off your original loan, you’re immediately eligible for a new loan. However, this isn’t recommended.

READ MORE: Can you have multiple payday loans?

Are tribal loans legal in Texas?

Native American tribes are sovereign nations in the United States. That means they’re generally immune to state regulations and it’s hard to sue them for breaching the laws of the states they reside in, though they usually follow applicable federal laws.

Tribal lenders are a type of short-term loan provider that partners with Native tribes to try and share in their tribal immunity. They use that as an excuse to sidestep the regulations meant to protect consumers, such as the rate restrictions on payday loans.

Tribal lenders are technically legal in Texas. There are no prohibitions on offering lending services out of a Native American reservation. However, all lenders must be licensed by the Texas Office of Consumer Credit Commissioner, and many tribal lenders do not hold the appropriate state licenses. Loans from unlicensed lenders may not be legally collectible. If you believe you’ve borrowed money from an unlicensed lender, don’t hesitate to contact a Legal Aid attorney for advice.

READ MORE: Is my payday lender licensed in my state?

Where to make a complaint

The Texas Office of Consumer Credit Commissioner is also the best place to lodge complaints about payday loan providers that operate within the state. Here’s the contact information:

- Regulator: Texas Office of Consumer Credit Commissioner

- Address: Finance Commission Building, 2601 N. Lamar Blvd., Austin, TX 78705

- Phone: 512-936-7600

- Link to website: https://occc.texas.gov/consumers/file-a-complaint

Consumers can also submit a complaint to the Consumer Financial Protection Bureau (CFPB). The CFPB is a federal organization whose purpose is to help consumers with their financial issues, including any problems with payday lenders.

Number of Texas consumer complaints by issue

These statistics are all according to the CFPB Consumer Complaint Database.

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 498 |

| Struggling to pay your loan | 330 |

| Can’t contact lender or servicer | 214 |

| Received a loan you didn’t apply for | 172 |

| Problem when making payments | 141 |

| Problem with the payoff process at the end of the loan | 106 |

| Can’t stop withdrawals from your bank account | 99 |

| Loan payment wasn’t credited to your account | 90 |

| Getting the loan | 85 |

| Incorrect information on your report | 82 |

| Charged bank acct wrong day or amt | 38 |

| Money was taken from your bank account on the wrong day or for the wrong amount | 31 |

| Applied for loan/did not receive money | 31 |

| Problem with additional add-on products or services | 26 |

| Problem with a credit reporting company’s investigation into an existing problem | 22 |

| Improper use of your report | 18 |

| Vehicle was repossessed or sold the vehicle | 18 |

| Credit monitoring or identity theft protection services | 4 |

| Vehicle was damaged or destroyed the vehicle | 3 |

| Unable to get your credit report or credit score | 3 |

| Property was sold | 2 |

| Property was damaged or destroyed property | 1 |

Source: CFPB website

The most common complaint consumers in Texas make to the CFPB is that their lenders charge unexpected fees and interest. That’s significant (if not surprising), but it’s not as notable as the sheer number of complaints.

The CFPB has received just under 500 complaints about this issue since 2013. These numbers make Texas the state with the second-most complaints in the nation overall.

The most complained about lender in Texas: CURO Group Holdings

CURO Group Holdings, also known as CURO Intermediate Holdings, is the lender that consumers complain about the most in Texas. CURO is a parent company for several different lending brands, including:

- Speedy Cash

- Rapid Cash

- Verge Credit

- Avio Credit

- Opt +

- Revolve Finance

While the last two in the list offer relatively harmless products and services (prepaid debit cards and online banking), the others sell usurious loans. The most well-known example is Speedy Cash, which has storefronts across the country.

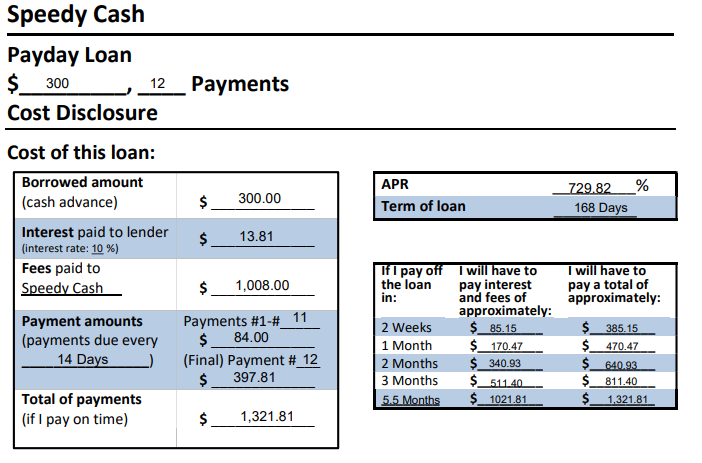

Speedy Cash’s rates and terms page is a helpful illustration of how credit access businesses work in Texas.

The sample cash advance is for $300. While the interest rate to the third-party lender is a reasonable $13.81, which works out to a 10% interest rate over the 168-day term.

However, Speedy Cash’s fees are a staggering $1,008 because there’s no limit to the amount they can charge. That works out to a 730% APR.

Most common complaints about CURO Group Holdings

| Complaint Reason | Count |

| Charged fees or interest you didn’t expect | 72 |

| Received a loan you didn’t apply for | 33 |

| Struggling to pay your loan | 31 |

| Can’t contact lender or servicer | 19 |

| Payment to acct not credited | 15 |

| Can’t stop withdrawals from your bank account | 11 |

| Incorrect information on your report | 10 |

| Problem with the payoff process at the end of the loan | 8 |

| Money was taken from your bank account on the wrong day or for the wrong amount | 8 |

| Can’t stop charges to bank account | 7 |

| Charged bank acct wrong day or amt | 7 |

| Getting the loan | 3 |

| Vehicle was repossessed or sold the vehicle | 2 |

| Applied for loan/did not receive money | 1 |

| Problem with a credit reporting company’s investigation into an existing problem | 1 |

| Credit monitoring or identity theft protection services | 1 |

| Loan payment wasn’t credited to your account | 1 |

| Was approved for a loan, but didn’t receive the money | 1 |

Source: CFPB website

In Texas, the most common reason people complain about CURO Group Holdings is that the lender charged them fees or interest that they didn’t expect. At this point, that should probably come as no surprise to you, though.

In addition to the sheer size of the fees that payday lenders like Speedy Cash charge through the credit access business loophole, the structure of these loans is extra confusing.

The average consumer isn’t likely to take the time to understand all of the nuances involved in the Texas payday loan laws. As a result, it’s all too easy for predatory lenders to blindside them with fees equivalent to more than $1,000 on a $300 loan.

Top 10 most complained about payday lenders

| Lender | No. of complaints since 2013 | Primary complaint reason |

| CURO Intermediate Holdings | 232 | Charged fees or interest you didn’t expect |

| Populus Financial Group, Inc. | 190 | Struggling to pay your loan |

| CNG FINANCIAL CORPORATION | 74 | Charged fees or interest you didn’t expect |

| ENOVA INTERNATIONAL, INC. | 74 | Charged fees or interest you didn’t expect |

| Cottonwood Financial Ltd. | 73 | Charged fees or interest you didn’t expect |

| Ad Astra Recovery Services Inc | 72 | Received a loan I didn’t apply for |

| Conn’s, Inc. | 57 | Problem when making payments |

| TMX Finance LLC | 50 | Struggling to pay your loan |

| COMMUNITY CHOICE FINANCIAL, INC. | 48 | Received a loan I didn’t apply for |

| Advance America, Cash Advance Centers, Inc. | 38 | Charged fees or interest you didn’t expect |

Source: CFPB website

CURO Group Holdings and its subsidiaries are far from the only lenders that consumers have problems with in Texas. In fact, there have been 676 complaints to the CFPB about the other lenders in the top ten least wanted list.

For most of these lenders, the most common complaints were about the high cost of the loans. Borrowers consistently reported being surprised by their charges and having difficulties keeping up with their loans.

If you’re struggling financially because you have payday loan debt with any of the lenders on this list, DebtHammer can help. Contact us for a free quote, and we’ll start working to get you out of the payday loan trap today.

Payday loan statistics in Texas

- Texas ranks as the 2nd state for the most overall payday loan complaints.

- Texas ranks as the 11th state for the most payday loan complaints per capita.

- There have been 18,281 payday loan-related complaints made to the CFPB since 2013―2,044 of these complaints originated from Texas.

- The estimated total population in Texas is 28,995,881 people.

- There are 7.0493 payday loan complaints per 100,000 people in Texas.

- The most popular reason for submitting a payday loan complaint is “Charged fees or interest you didn’t expect.”

READ MORE: Payday loan debt statistics

Historical timeline of payday loans in Texas

The Texas payday loan laws have never been very restrictive, but there have been some efforts to change that. Here’s a historical overview of the most significant developments in the area.

- 2001: The Texas Office of Consumer Credit Commissioner tries to lock down payday lending by implementing a 10% interest rate limit. However, it backfires, and lenders find the credit services organization loophole. It lets them charge fees virtually without restriction.

- 2011: “Credit services organizations” become “credit access businesses,” but they continue to operate the same way. Payday lending thrives in Texas.

- 2013: Legislation passes requiring payday lenders to post a schedule of their fees in a visible place, which helps prevent borrowers from misunderstanding the costs of a payday loan. Houston also passes the local payday lending regulations that limit their activities.

- 2015: There’s a significant push by legislators to address payday loans, but no legislation passes. It demonstrates the unlikelihood of stricter state regulations anytime soon.

In 2021, there’s still no sign of state legislature on the horizon that will plug the credit access business loophole. However, more than 45 cities in the state have adopted local regulations that limit their activities.

Austin, Dallas, Houston, and San Antonio are among them. You can keep up with the progress as the Texas Municipal League releases updates.

Flashback: A Texas payday loan story

It’s been illegal to arrest people for unpaid debts since the 1970s because of the Fair Debt Collection Practices Act. And yet, the year is 2015, and payday lenders are still using lawsuits and threats of jail to collect from delinquent borrowers.

When customers can’t afford the astronomical costs of these lenders’ payday loans, they start to receive intimidating calls and emails.

“A dirty trick employed by debt collectors is accusing borrowers of fraud. They’ll claim the borrower knew they wouldn’t pay back the debt, so they can go to jail for fraud,” says Austin-based criminal defense attorney Ben Michael. “Under the fair debt collectors act, collectors cannot threaten criminal charges. So file a complaint with your attorney general if this happens”.

These include threats of arrest, criminal charges, and jail time. While it’s rare, some small percentage of these people do end up going to jail. Payday lenders argue that these borrowers are committing check fraud.

They claim that the borrowers knew ahead of time their post-dated checks wouldn’t go through. As a result, the courts send letters to the borrowers warning them that they might face arrest if they don’t pay.

In the vast majority of cases, the lender then gets what they wanted in the first place: the borrower pays up, even if it means not putting food on the table.

In Collin County, Texas, 204 people paid a total of $131,836 to payday lenders after receiving notification that the payday lenders had filed criminal charges against them.

The bottom line: Should you take out a payday loan in Texas?

Payday lending is an usurious practice that often traps borrowers in a cycle of debt. Taking a payday loan is risky in the best circumstances, and the Texas payday loan laws are far from the best.

Even the slightly more strict local regulations ultimately do little to reign in the industry. Even if you desperately need financing, you probably shouldn’t take out a payday loan in Texas. It’s only going to make things worse.

There are more affordable forms of credit out there, even if you don’t have a good credit score. Consider using paycheck advance apps like Even or Dave to cover you in the short term.

They can get you a few hundred dollars advanced on your paycheck, are virtually free to use, and don’t check your credit. Of course, you can’t use debt to get by forever. Eventually, it’s going to catch up with you.

If you want to get out of debt and stay out of it for good, let us help. DebtHammer specializes in helping you fight back against predatory creditors like payday lenders.

Contact us for a free quote to get started today!