Debt consolidation loans can help make multiple high-interest debts more manageable by combining them into one simple monthly payment. Most of these loans aren’t guaranteed because they require a good credit score, but some lenders work with borrowers with a 520 credit score.

The best debt consolidation loans come with a lower interest rate than the original debts. They also often have a more reasonable payoff period and can be used to repay debt sooner. Before searching for a direct lender, you may want to try a lender matching service first for your best chances of finding a guaranteed debt consolidation loan.

Looking for a debt consolidation loan?

We may be able to help. It’s easy and free to find out.

Table of Contents

Lender matching services

Lender matching services are essentially websites or platforms that match you with the best lenders for your needs. They are not direct lenders, but they do partner with a network of lenders offering different types of financing.

These services use your information, such as credit score and basic contact info, to find the best loan options available. The application process is usually fast and free. Once the service has found the top lenders with the best match, you are then given a list of potential loan offers.

Included in these loan offers are:

- Loan amount

- Repayment terms

- Loan type (ex. debt consolidation)

- Expected monthly payment

- Interest rate

- Any other fees (ex. origination fee or prepayment penalty)

- Eligibility requirements (ex. minimum credit score or debt-to-income ratio)

You can compare the different options to determine whether your approval for a debt consolidation loan will be guaranteed. This is usually the easiest way to find a loan without searching for each lender separately.

After choosing a loan, you’ll be redirected to the lender’s site, where you can apply directly.

With that in mind, here are 10 almost guaranteed debt consolidation loans for borrowers with no (or low) minimum credit scores.

Disclaimer: Some or all of the products featured in this article are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. All opinions are our own.

Our top three lenders

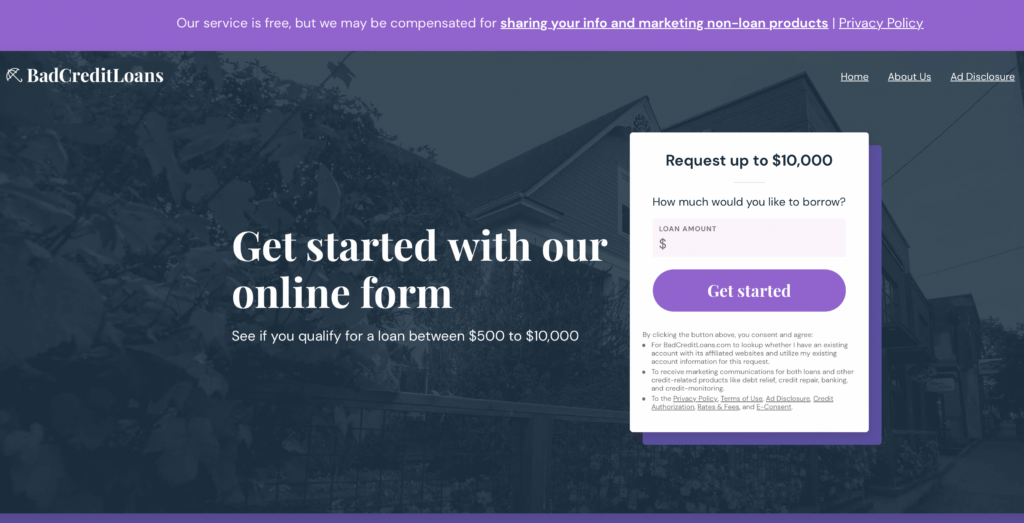

Best if you need a small loan: BadCreditLoans.com

- Loan amounts: $500 to $10,000

- Maximum loan: $10,000

- Loan terms: 3 to 36 months

- Interest rate: 5.99% to 35.99%

- Other noteworthy information: Many of the loans are customized based on the borrower’s needs and financial situation. The application process is more in-depth than similar platforms.

- Minimum credit score: It depends on the lender, but some lenders work specifically with individuals with bad or spotty credit histories.

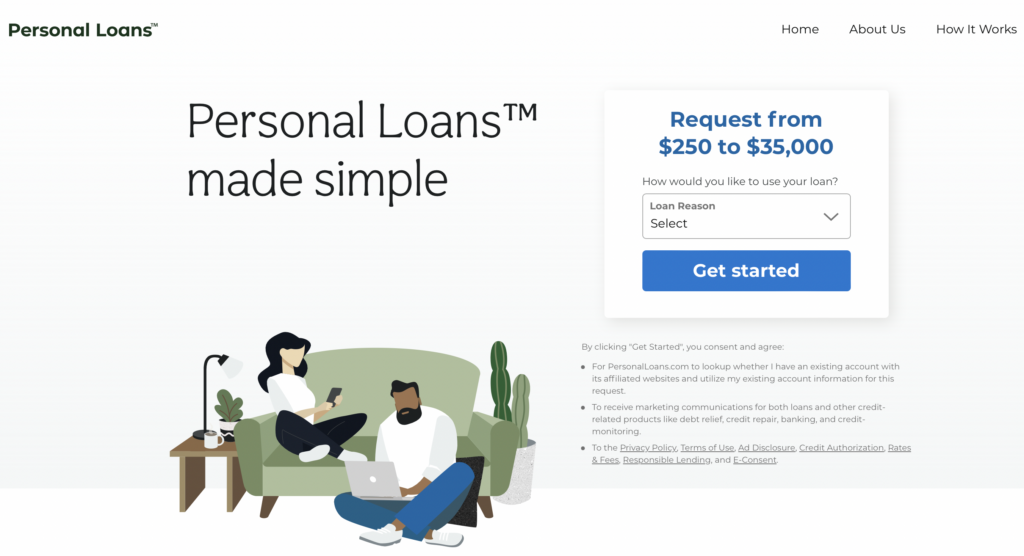

Best if your credit score is 580+: Personalloans.com

- Loan amounts: $1,000 to $35,000

- Maximum loan: $35,000

- Loan terms: 3 to 72 months

- Interest rate: 5.99% to 35.99%

- Other noteworthy information: The initial application is free, but some lenders charge other fees, such as a 1% to 5% origination fee. Personalloans.com is a member of the Online Lenders’ Alliance, meaning it uses fair and honest consumer practices. It offers a variety of loans, including installment loans, bank loans and peer-to-peer loans.

- Minimum credit score: Most personal loans require a 580+ credit score.

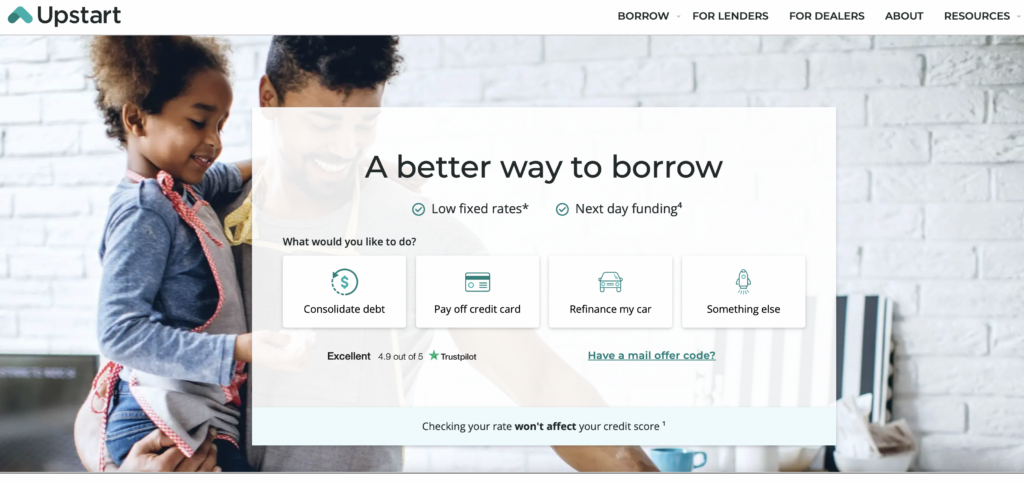

Best for large loans: Upstart

- Loan amounts: $1,000 to $50,000

- Maximum loan: $50,000

- Loan terms: 3 or 5-year terms

- Interest rate: 5.40% to 35.99% (fixed)

- Other noteworthy information: Upstart has an in-depth application process and a large network of reputable lenders. There are no prepayment fees, but there are late fees of up to 5% of the amount past due.

- Minimum credit score: Any credit score is OK. Some of Upstart’s partner lenders work with borrowers with a 300+ FICO score. Apply now! No credit score is required.

Seven more top lenders

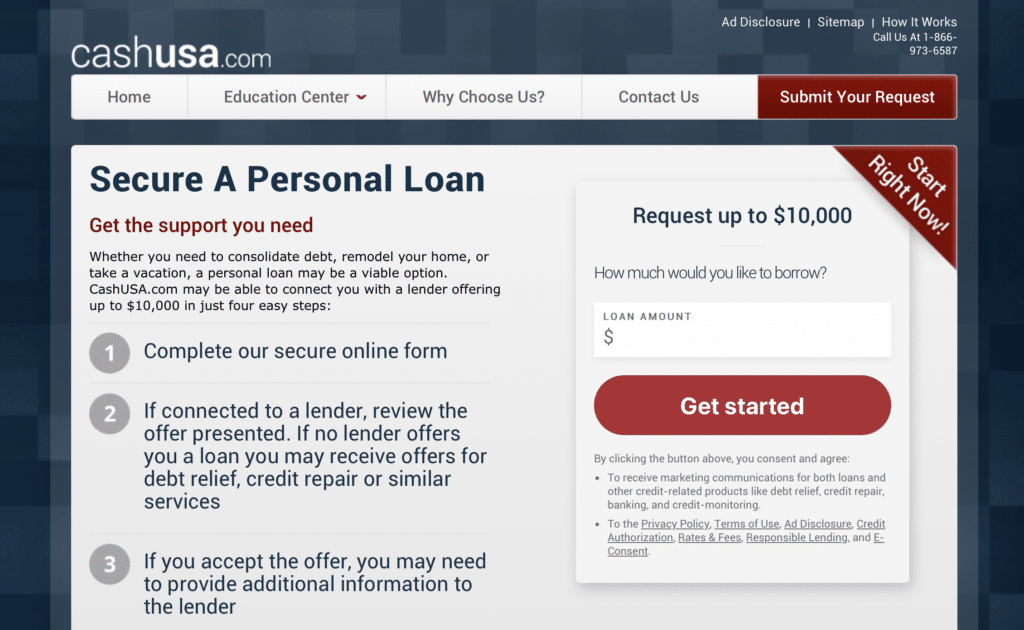

CashUSA.com

- Loan amounts: $500 to $10,000

- Maximum loan: $10,000

- Loan terms: 3 to 72 months

- Interest rate: 5.99% to 35.99%

- Other noteworthy information: It’s a simple online platform for getting a personal loan or debt consolidation loan. There’s a large network of partner lenders with different offers. Borrowers must make at least $1,000 a month to qualify. Some loans come with an origination fee, depending on the lender.

- Minimum credit score: All credit types are OK, but some lenders won’t work with poor credit borrowers. A bad credit score may also mean higher interest rates and lower loan maximums.

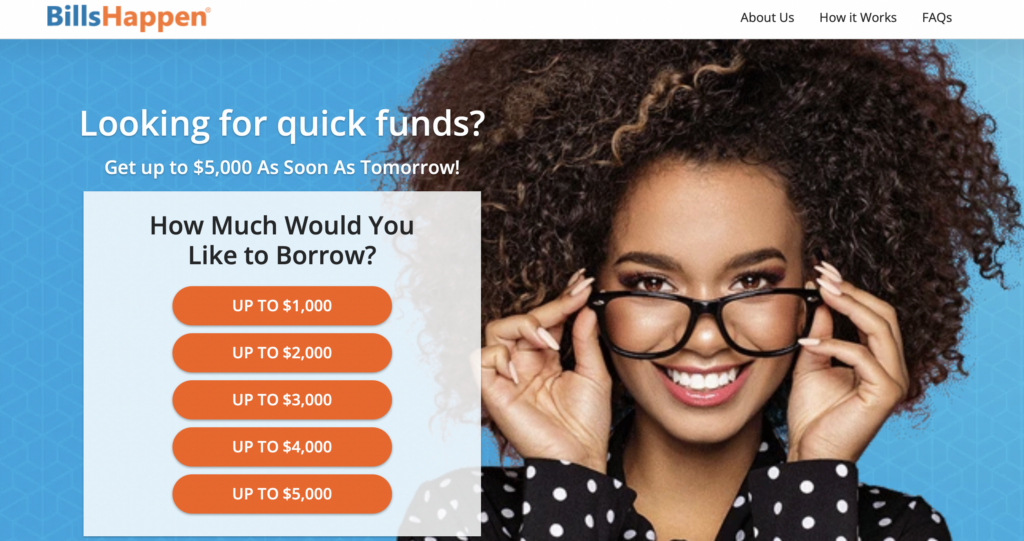

BillsHappen

- Loan amounts: $1,000, $2,000, $3,000, $4,000, and $5,000

- Maximum loan: Up to $5,000

- Loan terms: Starting at 3 months

- Interest rate: Variable (depends on the lender)

- Other noteworthy information: BillsHappen requires a basic application that includes the loan type and amount needed. It then redirects you to a lender they consider suitable based on that information. At this point, you will see the loan terms and other specific details that are available.

- Minimum credit score: Any credit score is OK, including bad credit. For the best rates, a credit of 670+ is recommended.

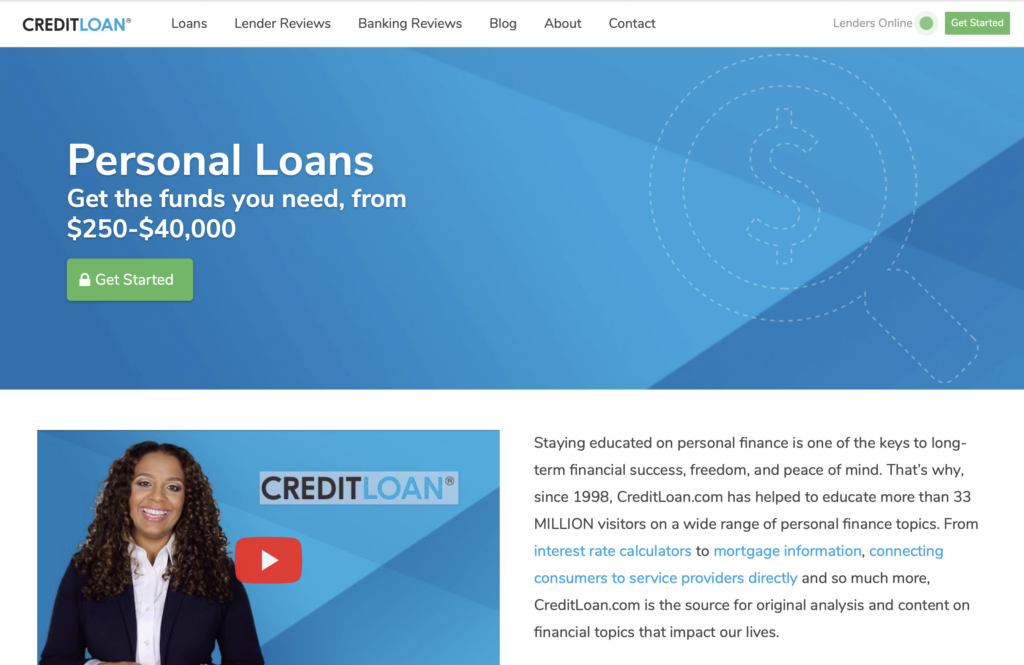

CreditLoan.com

- Loan amounts: $250 to $40,000

- Maximum loan: $40,000

- Loan terms: Usually 3 to 72 months (depending on the lender)

- Interest rate: Varies based on the lender and applicant’s credit score

- Other noteworthy information: This service partners specifically with lenders that work with bad credit borrowers. It also has some loans specifically for active or ex-military personnel. Funds may be available as soon as the next business day after approval.

- Minimum credit score: All credit scores are accepted, including bad credit (under 620).

P2PCredit

- Loan amounts: $1,000 to $40,000

- Maximum loan: $40,000

- Loan terms: 3 to 72 months with a biweekly or monthly payment

- Interest rate: 5.99% to 35.99%

- Other noteworthy information: Various loans are available, including debt consolidation and personal loans. During the application process, there are four credit score categories to choose from (Excellent, Good, Fair and Bad). Choosing one redirects you to a Reliable Personal Loans website where you can complete a loan application. Borrowers who’ve filed for bankruptcy in the past 7 years may not be eligible.

- Minimum credit score: This depends on the lender, but most require a 580+ credit score.

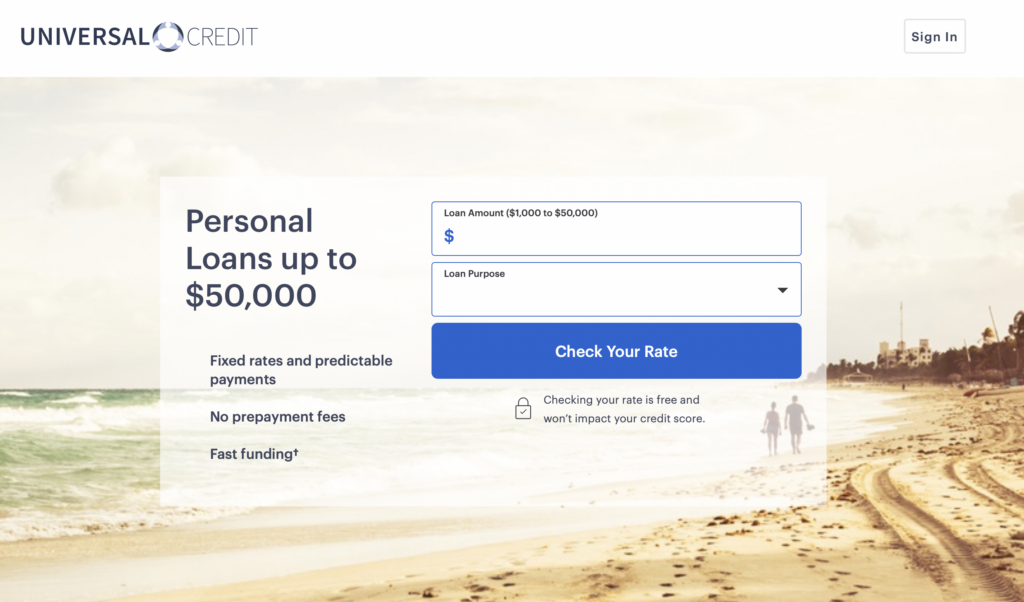

Universal Credit

- Loan amounts: $1,000 to $50,000

- Maximum loan: $50,000

- Loan terms: 36 to 60 months

- Interest rate: 11.69% to 35.93% (fixed rate)

- Other noteworthy information: This service partners with Cross River Bank and Blue Ridge Bank to provide personal and debt consolidation loans. The loans come with a 5.25% to 8% origination fee. There are no prepayment penalties or other fees.

- Minimum credit score: Universal Credit requires borrowers to have a 560 FICO score or above.

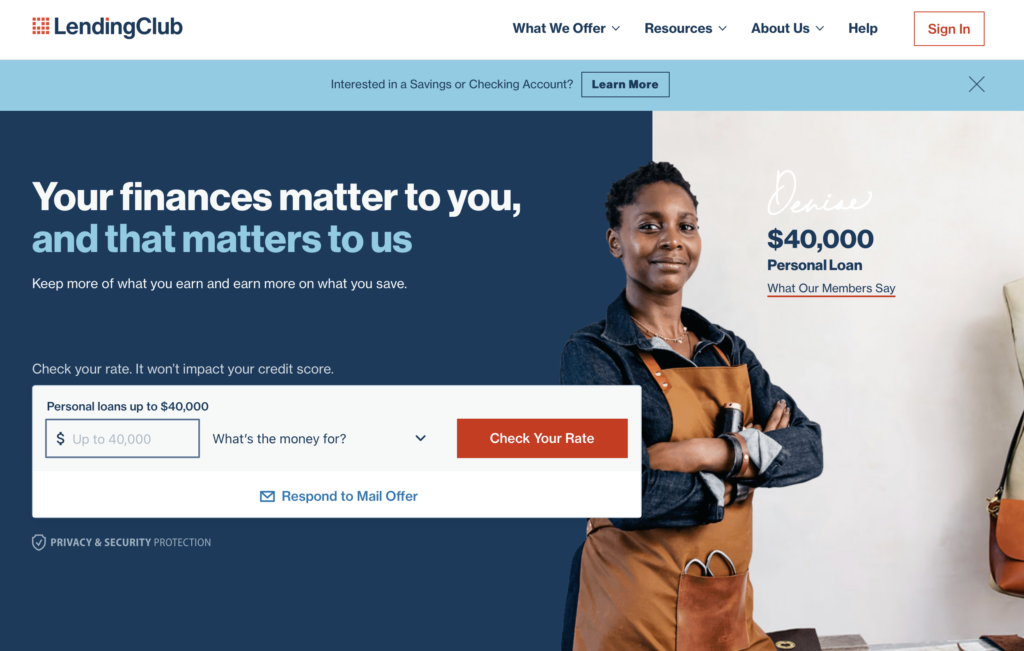

Lending Club

- Loan amounts: $1,000 to $40,000

- Maximum loan: $40,000

- Loan terms: 36 to 60 months.

- Interest rate: 6.34% to 35.89%

- Other noteworthy information: There is a 2% to 6% origination fee. There are no application or pre-payment fees. Funds are available as soon as one business day after approval.

- Minimum credit score: Lending Club has a minimum credit score of 600.

Upgrade

- Loan amounts: $1,000 to $50,000

- Maximum loan: Up to $50,000

- Loan terms: 24 to 84 months

- Interest rate: 8.49% to 35.97%

- Other noteworthy information: There’s a 2.9% to 8% origination fee with most personal loans. There are no pre-payment fees. There’s also an Upgrade Visa card that has 1.5% unlimited cashback rewards.

- Minimum credit score: Upgrade’s minimum credit score is 560 FICO.

READ MORE: Debt consolidation loans for married couples

How debt consolidation works

Debt consolidation combines two or more unsecured debts, like credit cards, into a personal loan. Individuals may apply for a larger loan to cover these smaller debts, so they have one loan instead of multiple loans. They must then repay the new loan as usual, typically in fixed monthly installments.

There are many reasons to consolidate debt, including:

- Have one monthly payment instead of multiple

- Get a lower interest rate (based on credit)

- Pay down debt faster or on a fixed schedule

READ MORE: Debt consolidation for military vets

Borrowers with high-interest debts like payday loans or credit cards can usually save money with debt consolidation.

The process of consolidating debt is fairly simple. Start by making a list of any current debts you want to combine. Include the monthly payments and interest rates. Then, calculate how much you’re paying each month for those debts. Add up the remaining balances on all of the accounts.

When in doubt, use an online debt consolidation calculator. This can show you whether debt consolidation is the best option for you and if it fits into your budget and financial goals.

READ MORE: Debt consolidation pros and cons

What happens if I have bad credit?

Even borrowers with bad credit can still get debt consolidation loans. It does depend on the lender, though. It may also depend on other factors, like the borrower’s income and total debt-to-income ratio.

If you have bad credit (629 FICO and below), here’s what to do:

- Fill out an application with a legitimate lender matching service. Include any details such as full name, date of birth, military status, employment status, credit score, income, contact info, the amount needed, etc.

- Review the loan offers and lenders. Look for competitive rates and repayment terms. See if they offer any discounts for autopay or if there are hidden fees (ex. prepayment fees). Check the minimum and maximum loan amount.

- Go through the prequalification process. Prequalifying for a loan doesn’t affect your credit score and can give you an idea of the loan you could get. Include the amount you need to borrow, accounting for any origination fees or prepayment charges.

- Apply. After finding the ideal lender and loan offer, move forward with the loan application process.

- Look over the loan offer. Once qualified, you’ll receive the specific details about the loan. This includes things like the loan amount, loan term, monthly payment and annual percentage rate (APR). Review everything to make sure it’s what you want and need.

- If the terms are reasonable to you, sign the loan agreement. At this point, the funds (minus origination fees) will be deposited into your bank account. Many lenders offer same-day or next-day funding after approval.

- Use the new loan to pay off existing debts. Focus on consolidating the debts with higher interest rates and/or amounts.

- Double-check the consolidated account balances. Make sure the old loans or credit cards have a zero balance. If there is still a balance, repay it as soon as possible to avoid accruing interest or late fees.

- Focus on repaying the debt consolidation loan. There should be just one monthly payment to manage now. Keep up on payments; if there’s no prepayment penalty, try to pay more than the minimum. The sooner you pay off the new loan, the sooner you’ll be out of debt.

- Avoid accumulating more debt. Try not to use any credit cards you still have unless it’s an emergency. Avoid taking out new loans, too.

READ MORE: How does divorce affect debt consolidation?

What credit score do I need for a debt consolidation loan?

There’s no set minimum credit score for a debt consolidation loan. Many lenders require a minimum FICO score of 620, but some will approve applications from borrowers with lower scores (e.g., 520 FICO).

Each lender uses its own criteria to assess the applicant’s creditworthiness, so shop around until you find the best one.

READ MORE: Debt consolidation loans while unemployed

Do debt consolidation loans hurt your credit score?

When you apply for a loan, the lender will request your credit report from one or more credit bureaus. This will result in a hard pull or inquiry and temporarily lower your credit score by five to 10 points.

Prequalification is another option that includes a soft pull of your credit history. This will show up on your credit report, but it will not affect your credit score. It’s a good option for those who want to compare loans before choosing one. Once you select a specific loan, the lender will still perform a hard inquiry.

Besides this, a debt consolidation loan’s only real negative impact is if you fail to make the monthly payments on time.

READ MORE: Does debt consolidation close credit cards?

Debt consolidation can help your credit score

Debt consolidation can help your credit score in a few ways. These include:

- Reducing your debt-to-income ratio and credit utilization rate

- Adding to your mix of credit

- Making on-time payments consistently (this can help your payment history)

The negative effects of debt consolidation, such as opening a new account or the hard inquiry, are usually temporary. This means your score will bounce back after a few months or so with other good credit habits.

READ MORE: Four ways debt consolidation affects your credit score

Other loan options

Besides debt consolidation, here are a few other viable options for paying down debt and building credit:

- Co-Signer: A co-signer is someone who signs for a loan with the primary borrower. This can improve the borrower’s chances of qualifying for a loan since the lender will also consider their income and credit score. The co-signer is responsible for making payments if the primary borrower fails to do so.

- Payday Alternative Loan (PAL): Offered by federal credit unions, this short-term loan can be used to consolidate smaller debts. PALs come in amounts ranging from $200 to $2,000. They have 1- to 12-month repayment periods.

- Mortgage Refinance, home equity loan or line of credit: Homeowners with equity in their home may be able to refinance their mortgage to get a lower interest rate. This can free up some money to tackle other debts. Alternatively, they can take out a home equity loan or line or credit to consolidate other debts. The biggest drawback is that defaulting on the new loan could mean losing the home.

- Secured loan: These are backed by collateral, such as a car. They’re a good option for borrowers with poor credit who need a loan. However, if the borrower defaults on the loan, they could lose the collateral.

- Balance transfer credit card: This credit card lets you transfer debt from one high-interest credit card to another, ideally with lower interest. Some of these cards come with a 0% introductory APR that lasts 12 to 21 months, on average. If you pay off the entire balance in that time, you won’t have to pay interest.

READ MORE: Debt consolidation loans for health care workers

Other debt relief options

Looking for debt relief instead of guaranteed debt consolidation loans? Here are the best options:

READ MORE: Pros and cons of debt settlement

The bottom line

There are debt consolidation loans for borrowers with any type of credit. These loans can make it easier to manage existing debts and potentially pay down debt faster. If debt consolidation isn’t right for you, other options for debt relief exist, such as credit counseling, secured loans and mortgage refinancing. Weigh your options and choose the one that best fits into your budget and goals.