Updated March 7, 2024, to include a class action lawsuit filed against FloatMe in Pennsylvania.

FloatMe is a paycheck advance app that loans (or “floats”) you extra cash until payday. You can use the money however you need to, whether to buy groceries, fill up the gas tank or pay a bill.

The app has some features that make it unique, but one particular drawback is the $50 limit. Here’s what you need to know if you’re considering a cash advance from FloatMe.

Our take: FloatMe offers convenient cash advances of up to $50, but the low initial advances (as low as $10) combined with the monthly fee make this an expensive borrowing option compared to similar apps. If you’re paying $4 per month to borrow $10, that’s a 1042% APR. That’s significantly more than what most payday lenders would charge. You’re better off choosing an option with a lower monthly fee and higher initial borrowing amount.

Table of Contents

What is FloatMe?

FloatMe is not a lender or a provider of loans. It’s an app that offers small paycheck advances capped at $50. While most cash advance apps offer advances ranging from $200 to $500, FloatMe subscribers can’t borrow more than $50, and you can’t have more than one advance at a time.

When your FloatMe advance is approved, the money will be transferred directly to your bank account. You will repay it on your next payday.

Pro tip: Don’t expect to be eligible for the full $50 the first time you request an advance. Eligibility will be based on your banking history, but most new customers start with “floats” of $10 to $20. According to the Federal Trade Commission, only .05% of users are immediately eligible for a $50 float.

How FloatMe works

FloatMe works by connecting to your bank account and analyzing your transactions. If you meet their criteria, you will be approved for a “float.” The amount of the float will be automatically deducted from your next paycheck’s deposit.

FloatMe charges a monthly subscription fee of $3.99. That’s high in proportion to the maximum amount of money you can borrow, and the fee has doubled since DebtHammer last assessed the company in 2022.

Pro tip: For borrowers who are only eligible for a $10 float, that’s an annual percentage rate equivalent to 1042%, and that’s if you wait three business days for the money to be transferred. If you can borrow the full $50, you’re paying the equivalent of a 208% APR (not counting any additional fees to expedite the transfer.)

FloatMe only works with employed people who receive W-2 forms. Unfortunately, this means that gig workers and the self-employed are unlikely to be eligible for floats.

FloatMe’s key features

- FloatMe doesn’t charge interest: FloatMe will withdraw the loan from your next paycheck, but if you can’t afford to pay back the entire $50 lump sum, you can make arrangements for a partial payment to prevent an overdraft.

- Membership fee: FloatMe charges a membership fee (they call it a “connection fee)” of $3.99 a month to qualify for “floats,” but you can cancel at any time.

- Fast funding: It can take up to three business days to get your float, but depending on your bank, you may be able to get the money within an hour.

- Low borrowing amount: You’ll probably only be eligible to borrow between $10 to $30 to start. The loans max out at $50.

- No credit check: FloatMe doesn’t care about your credit history, and a hard pull won’t drag your score down when you apply.

- You must have a W-2: Self-employed workers aren’t eligible. Borrowers also must earn at least $200 per paycheck, which must be directly deposited into a bank account.

- Keeps tabs on your bank balance: FloatMe will monitor your bank account and alert you when your balance is low so you can avoid overdraft fees.

- Bank account access: Remember that FloatMe will have access to your account and will automatically debit you when your payment is due.

- FloatMe won’t help you build credit: Because FloatMe doesn’t report payments to any of the three major credit bureaus, the loans won’t help improve your credit history — even if you make your payments on time.

- Helps you build savings: FloatMe has some features that can help you set aside a small bit of money each payday in order to build a small emergency fund.

Pros and cons of FloatMe

FloatMe has a few advantages and disadvantages.

Pros

- No credit check

- Bank account monitoring

- No interest rates or late fees

- No tips

- 30-day free trial

- Automatic savings

- Overdraft alerts

Cons

- The $3.99 monthly subscription fee is high in proportion to the amount of money you can borrow

- Low borrowing maximum of $50

- High fees if you need instant transfers

- No due date extensions

- It won’t help build your credit score

- No contact information on the website

- Requires Plaid

- Customers say it’s difficult to cancel subscriptions

- No credit builder products

FloatMe’s requirements

Not everyone is eligible for Floats. There are some basic requirements to meet. These include:

- You must have direct deposits from your employer

- You must earn a minimum income of at least $200 per paycheck

- You must have a positive bank account balance

- Your checking account must have a debit card attached

- You must receive a W-2

Pro tip: Those who are self-employed or contract workers won’t qualify for FloatMe.

Other features

FloatMe offers overdraft alerts that will warn you whenever you’re close to exceeding your bank balance.

The other feature, FloatMe Stash, is a bit less clear-cut.

On June 11, 2020, the company announced the introduction of FloatMe Stash as a tool that helps you automate savings. You can read the announcement here.

A few months later, on Sept. 30, 2020, another announcement from the company stated that FloatMe Stash was being taken offline for upgrades based on customer feedback. It’s unclear if FloatMe Stash 2.0 is currently available. The company has not responded to requests for information on the status of the feature, and the website contains no mention of it.

The FloatMe experience

First, you’ll need to download the mobile app for your phone. Though FloatMe has a web presence, you can only access your account via a mobile device. It is available for IOS and Android.

Before you can use FloatMe, you’ll need to create an account. They tell you that your “first week is free” but that when that week is over, they’ll be charging you $3.99 per month to use their service.

Creating your account means giving the company basic information (legal name, address, and phone number) and connecting your bank account via the Plaid platform. You’ll also be asked to choose a minimum balance for your bank account. This is so the app can notify you if your balance falls below the specified amount. Once all of that is done, you can request your first float.

How long does it take to get your float?

That depends on how well your bank and FloatMe communicate. Some users can get their floats almost immediately. Others take a couple of days to show up. When you first sign up for the app, doing a test float might be worth it. That way, you can see how long it will take for future floats to arrive.

FloatMe charges a hefty fee if you need your advances immediately. Instant Float fees range from $3 to $5.

- $10 Instant Floats: $3.00 fee

- $20 Instant Floats: $4.00 fee

- $30+ Instant Floats: $5.00 fee

This is very high considering the small amount of money you can borrow. When combined with the monthly fee, you could pay $6 to have $10 instantly transferred to your bank account. You’re far better off asking a friend to float you $10 at that point.

Is FloatMe secure?

FloatMe requires your bank information to verify your income, send Floats to your account and withdraw repayment for the floats on their due date.

FloatMe uses the same systems and security as many banks and other finance products you know to securely connect your bank account to the app.

Does FloatMe use Plaid?

FloatMe uses Plaid to connect your bank accounts. Plaid is a service that securely connects your bank accounts to various apps. 12,000+ banking institutions around the world use it. Unfortunately, not all financial institutions are compatible with Plaid. Chase, Capital One, and PNC are among the major banks that don’t work with Plaid. If you bank through one of these, you must switch banks to use FloatMe.

How to cancel FloatMe

To stop automatic charges for the monthly fee, you must close your FloatMe account. You can close your account through the FloatMe mobile app or by contacting floatme.zendesk.com. Many customers have complained that closing the account through the app is complex and that the button doesn’t always work. In that case, your best bet will be to contact the company directly. Otherwise, the fee will continue to be debited from your linked account.

Pro tip: If you simply uninstall the FloatMe app, your account will not be closed, and you will continue to be charged the $3.99 monthly fee.

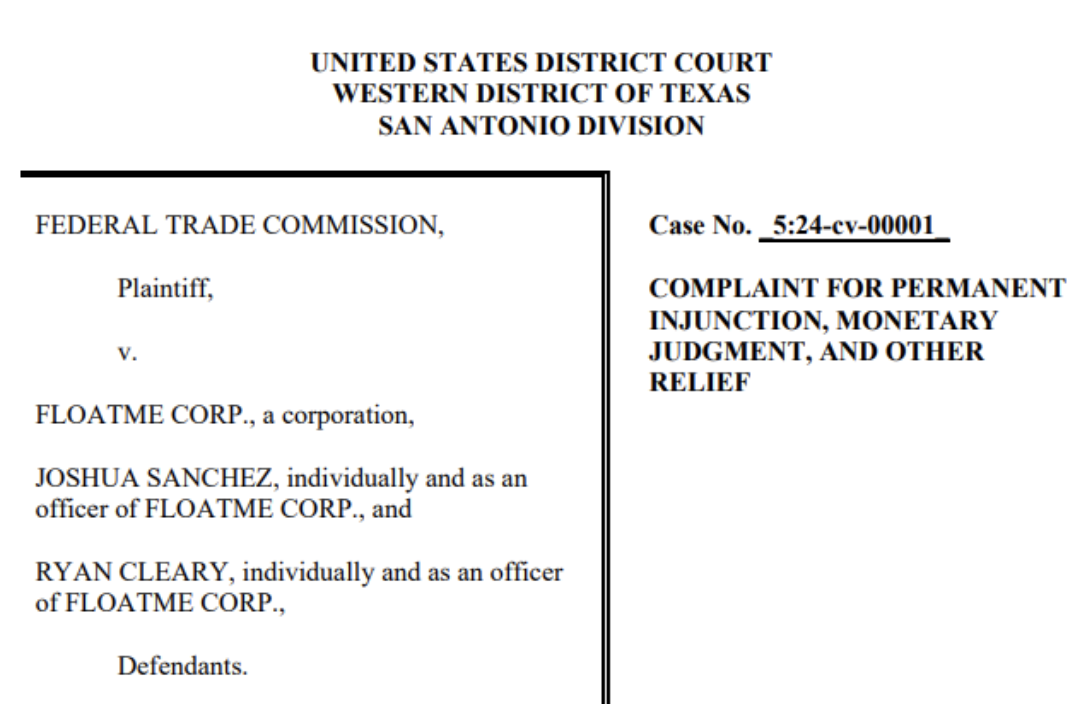

FloatMe’s legal challenge

In January 2024, the Federal Trade Commission sued FloatMe and its co-founders.

The FTC alleges FloatMe used “patterns designed to thwart … attempts to cancel” and charged users without their consent.

The lawsuit says FloatMe lured customers with promises of $50 Floats, but only .05% of customers could borrow the full $50.

The FTC also alleges that FloatMe’s cofounders knew FloatMe was “double or triple” charging subscription fees but didn’t immediately fix the issue.

FloatMe was also named in a class action lawsuit, Pierce et al. v. FloatMe Corp., filed on February 28, 2024, in Pennsylvania. The case alleges FloatMe charges rates higher than legally allowed in the state, citing more than 1,000% APR equivalents.

Customer ratings

- BBB accredited? No

- BBB rating: B

- BBB customer reviews: 3.15 of five stars

- Apple Store score: 4.8 out of five stars in more than 69,000 reviews

- Google Play score: 4.4 out of five in more than 42,000 reviews

Customer opinions

Reviews are mixed but generally positive.

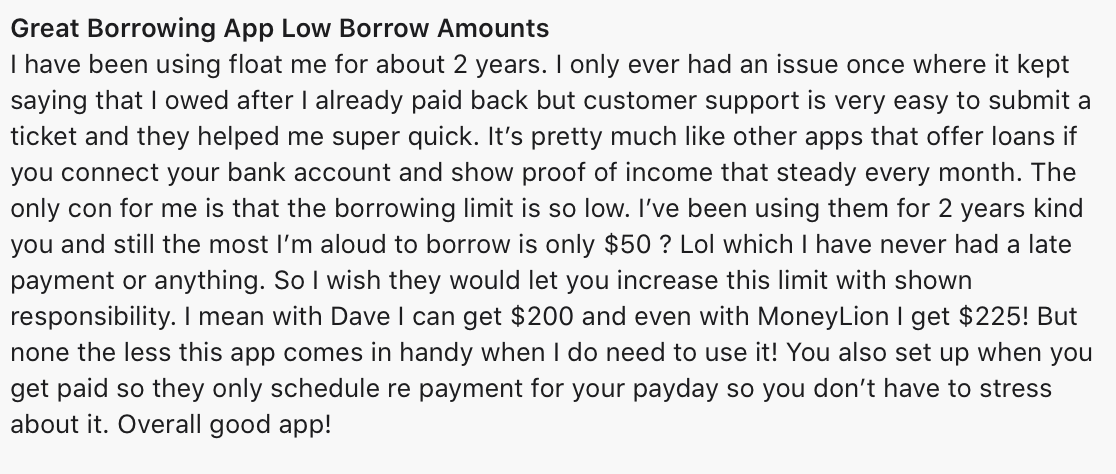

Most helpful FloatMe reviews

Complaints focus mostly on the low borrowing maximum, high fees, charges that continue to be withdrawn from bank accounts after the FloatMe account has been closed and inability to reach anyone from customer service when they encounter a problem.

But there are also plenty of people who are satisfied with the app.

From Apple’s App Store:

From Google Play:

From the Better Business Bureau:

There are also quite a few unhappy customers on pissedconsumer.com, where the site has earned 1.3 stars out of five, and 90% of reviews are complaints about the user experience. However, it’s also worth noting that this site draws unsatisfied customers almost exclusively.

At a glance: FloatMe vs. payday loans

| FloatMe | Payday loans |

| Maximum advance of $50 | Typically as high as $1,000 |

| Up to three business days unless you pay a fee for instant transfers | Next business day |

| The mobile app requires a linked bank account and debit card | Fees range from $15 to $25 for each $100 borrowed |

| Fees range from $15 to $25 for each $100 borrowed | Fees ranging from $15 to $25 for each $100 borrowed |

| Available to residents of 49 states (not available in Connecticut) | Not available in states where payday loans are illegal |

| No loan extensions | May be eligible for an extended payment plan |

The bottom line

FloatMe is a convenient option if you need to borrow a small amount of cash but can afford to wait a few days for it to post to your account. However, the extreme borrowing cap and high fees for immediate transfers mean it may not be a practical long-term solution, and the legal challenge from the FTC is cause for concern.

If you periodically need cash advances, and $50 just won’t cut it, you may be better off signing up for an app like FloatMe, but choose one with a lower monthly subscription fee or a higher borrowing maximum.

FAQs

FloatMe was founded in 2018 by Christopher Brown, Joshua Sanchez and Ryan Cleary.

FloatMe does not list a phone number. Instead, they direct customers to the support page on their website. FloatMe can also be contacted via email at [email protected]. The mailing address is 110 E Houston St, 7th Floor, San Antonio, Texas 78205

Other apps that will loan you some quick money (but don’t charge interest) include Dave, Brigit, MoneyLion, Earnin, Cleo, Empower and Chime. Learn more about these apps here.